Berkshire Hathaway: Never Bet Against Buffett

Alex Wong

Despite its size, Berkshire Hathaway (NYSE:BRK.A)(NYSE:BRK.B) was able to grow its business at an impressive rate in recent months thanks to the overall improvement of the American economy. Even though investors are now thinking about whether Berkshire Hathaway has additional room for growth in light of the passing of Charlie Munger a few months ago, I would argue that the company has everything going for it to continue to create additional shareholder value even if Warren Buffett is no longer in charge.

After spending decades building Berkshire Hathaway, Warren Buffett made the company a formidable cash cow machine that is more than likely to thrive even in turbulent times and under different leadership in the future. Therefore, I continue to stick with my BUY rating as it appears that nothing can undermine Berkshire Hathaway’s growth story for now.

Berkshire Hathaway Is Unstoppable

Back in November, I wrote a bullish article on Berkshire Hathaway where I argued that despite trading at its all-time highs, the company’s shares have additional room for growth. Since that time, Berkshire Hathaway’s stock has appreciated by ~17% and there’s an indication that the upside is still there.

The latest earnings report that was released last month showed that in Q4, Berkshire Hathaway’s operating income was $8.48 billion, an increase from $6.63 billion a year ago. At the same time, the FY24 operating earnings increased by 21% to $37.35 billion.

Such results in part were achieved thanks to the better-than-expected performance of Berkshire Hathaway’s insurance business. In 2023, the insurance underwriting after-tax earnings were $5.43 billion against a $30 million loss in 2022, while the margins were one of the highest in recent years. Going forward, it’s likely that the insurance business will retain its momentum in 2024 and continue to generate record earnings thanks to the expected growth of premiums that will positively affect Berkshire Hathaway’s overall performance.

When it comes to Berkshire Hathaway’s investing portfolio, it’s safe to assume that a significant portion of stocks from that portfolio will be able to continue to create additional shareholder value in years to come. While Berkshire Hathaway’s investment and derivative gains increased to $29.1 billion in Q4 in part thanks to the improvement of the overall macroeconomic environment, it’s safe to assume that stocks from the company’s portfolio will continue to benefit from macro tailwinds in the coming quarters. There’s already an indication that the U.S. economy will retain its momentum in 2024 as consumer spending is expected to remain robust.

At the same time, Berkshire Hathaway’s biggest holdings themselves have various growth catalysts that could unlock additional value in the coming months. Apple (AAPL), which is Berkshire Hathaway’s biggest holding, has managed to start its fiscal year on a high note thanks to the launch of the latest iPhones, and the expected release of newer MacBooks and iPads should help the company meet its guidance for the coming quarters.

Berkshire Hathaway’s major energy holdings such as Chevron (CVX) and Occidental Petroleum (OXY) are also expected to benefit from the latest bump in oil prices caused by various geopolitical factors. On the international front, Berkshire Hathaway’s successful investments in the biggest Japanese trading houses are giving Warren Buffett’s firm the ability to diversify its investment portfolio and offset the risks of its domestic holdings.

Considering all of this, I would say that Berkshire Hathaway’s growth story is far from over and there are reasons to believe that its stock has more room for growth. This is due to the fact that at the end of Q4, Berkshire Hathaway had $167.6 billion in cash reserves that could be deployed at any moment to expand the investment portfolio and drive operating income higher.

What’s more is that Berkshire Hathaway could be considered an even better investment than the Big Tech behemoths, which were mostly responsible for the overall market rally in the recent year. While Berkshire Hathaway is not a pure tech play, its significant position in Apple nevertheless exposes it to both the upsides and downsides of the tech industry, which has recently benefited from the growth of generative AI.

While Apple is relatively late to the party, there’s an indication that the company plans to capitalize on various generative AI opportunities in the foreseeable future. Last month it was reported that Apple plans to launch an alternative to Microsoft’s (MSFT) successful chatbot Copilot, while later Tim Cook announced that the company will break new ground in generative AI this year. Then earlier this month Bloomberg reported that Apple is in talks to integrate Google’s (GOOG)(GOOGL) Gemini AI engine into iPhones, while the company itself announced a couple of days ago that it will host the upcoming developers conference in June where a lot of new generative AI tools and products could be revealed.

If the AI rally continues, then Berkshire Hathaway will be able to continue to benefit from it thanks to its sizable holding of Apple’s shares. However, if the AI rally loses its momentum, Berkshire Hathaway would be in a position to mitigate the downfall thanks to the great diversification of its portfolio.

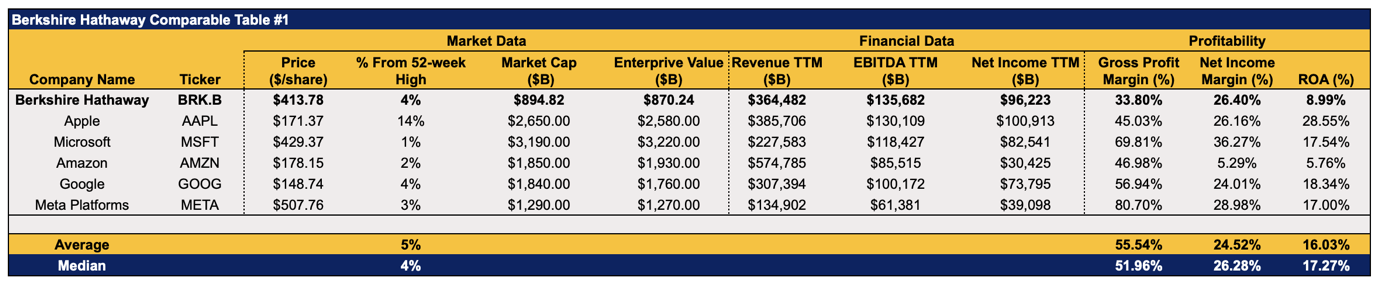

Berkshire Hathaway’s Comparable Table (Data: Seeking Alpha, The Table Has Been Made By The Author)

{kind=link}

From the valuation perspective, Berkshire Hathaway also trades at lower multiples in comparison to the major Big Tech companies. While some might argue that it’s best to compare Berkshire Hathaway to other conglomerates, the reality is that there is no other company of such a size that has a significant interest in private utilities, insurance, railways, and energy businesses, along with a sizable derivatives and investment portfolio.

By being a one-of-a-kind enterprise, I would say that it makes sense to compare Berkshire Hathaway to the biggest public companies in the world as it itself is close to reaching a $1 trillion valuation in the following months. That’s one of the main reasons to believe that Berkshire Hathaway might be a more attractive investment in the current environment than Big Tech stocks. At the same time, Berkshire Hathaway could also be considered undervalued against the broader market and be a great value play at the current price. That’s because the company trades at ~22 times its forward earnings, which is below the average forward P/E ratio of the S&P 500 index of ~28x. Therefore, it’s safe to assume that the upside in Berkshire Hathaway’s stock is still there.

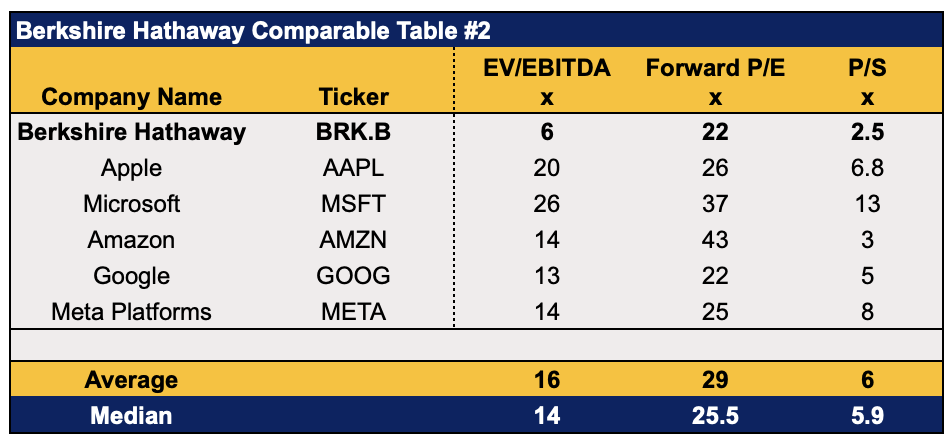

Berkshire Hathaway’s Comparable Table (Data: Seeking Alpha, The Table Has Been Made By The Author)

{kind=link}

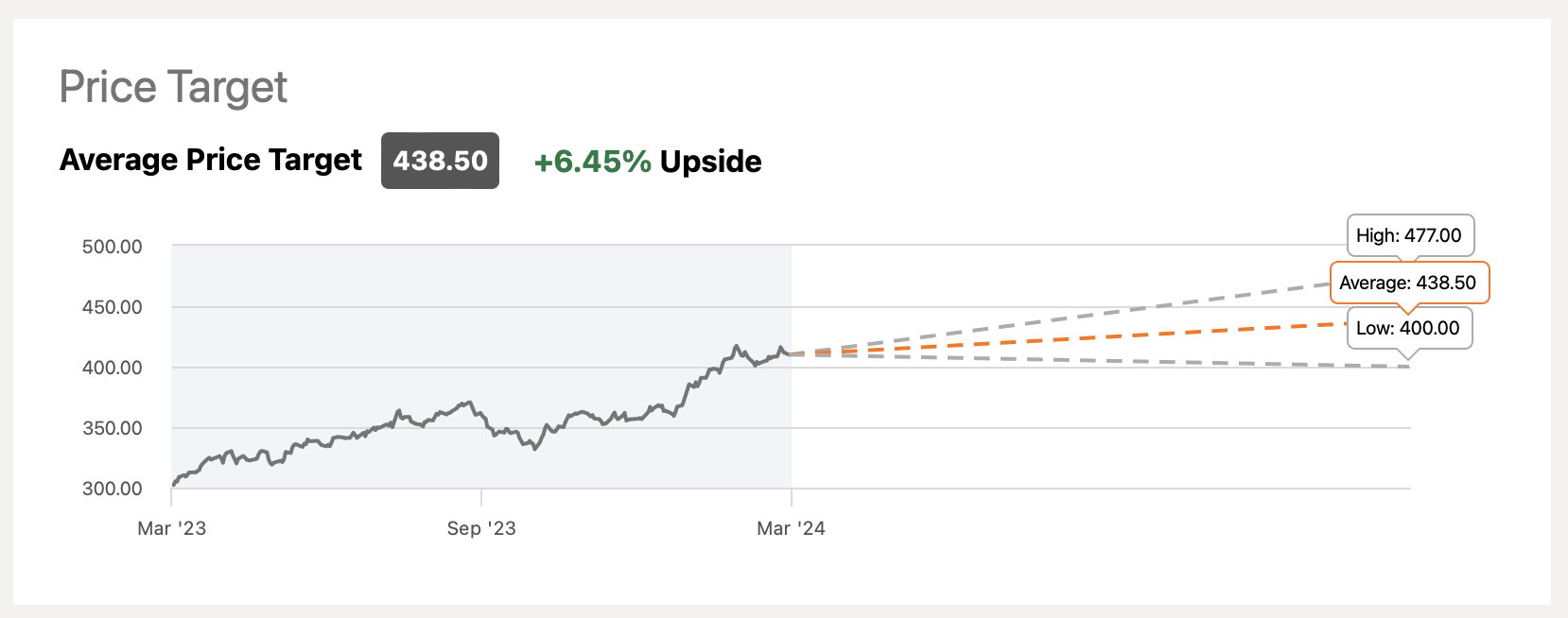

The street shares a similar sentiment and believes that after aggressively appreciating and reaching its all-time high levels in recent months, Berkshire Hathaway’s stock still has a decent upside.

Berkshire Hathaway’s Consensus Price Target (Seeking Alpha)

{kind=link}

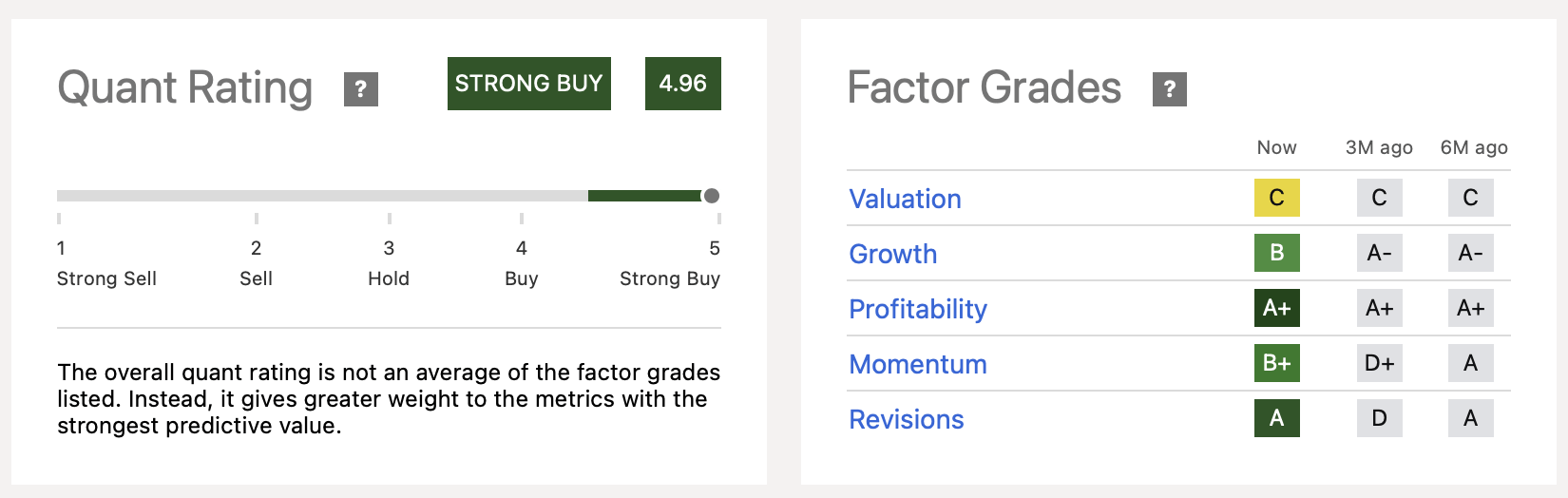

Seeking Alpha’s Quant System is also bullish about Berkshire Hathaway and is currently giving its stock a rating of Strong Buy.

Berkshire Hathaway’s Quant Rating (Seeking Alpha)

{kind=link}

Major Risks To Consider

While there are reasons to believe that Berkshire Hathaway’s growth story is not over yet and its stock appears to be a great value play, there are nevertheless several major risks that are associated with investing in the company. First of all, due to the changing regulatory climate, the earnings of Berkshire Hathaway’s Energy business declined by 40% to $2.3 billion last year, while Warren Buffett raised the possibility of bankruptcy of utilities in certain states in his latest letter to shareholders.

As for the investment and derivatives portfolio, Warren Buffett in his latest letter has also admitted that it would be harder to find companies that could truly move the needle at Berkshire Hathaway due to the business’s scale. While Berkshire Hathaway has immense resources and the ability to deploy capital at a large scale, there are only a handful of businesses that could have a meaningful impact on the overall performance of the conglomerate.

There’s also a risk that after being a great investment in the last half a decade, Apple could start underperforming in the foreseeable future due to the China-related risks that could undermine Tim Cook’s efforts to revive growth.

Last but not least, there are questions about whether Berkshire Hathaway would be able to thrive once Warren Buffett is no longer in charge of the firm. I would argue that by nominating his successor before giving up the reins of the firm, Warren Buffett is ensuring that the transition will be smooth and have little effect on the company’s operations. While Berkshire Hathaway’s stock is likely to depreciate in the short term when Warren Buffett retires or passes away, it will likely recover and continue to create additional shareholder value. This is due to the fact that Berkshire Hathaway will remain a formidable cash cow machine that is more than likely to thrive even in turbulent times and under different leadership.

The Bottom Line

Berkshire Hathaway was able to weather a turbulent macroeconomic and geopolitical environment in recent years and generate impressive returns. While some risks remain, it’s safe to assume that the worst is likely behind us, and the company has everything going for it to continue to create additional shareholder value. As such, I continue to rate Berkshire Hathaway as a BUY as there’s nothing to suggest that the company won’t be able to generate impressive returns even if Warren Buffett is no longer in charge.