Federal Reserve Watch: There Is Still Plenty Of Money Around

Grandbrothers

In the past banking week, the week ending Wednesday, June 26, the Fed’s securities portfolio declined by $18.2 billion.

This brings the reduction over the past four banking weeks, from May 29 through June 28 to a total of $54.5 billion.

And, since the quantitative tightening began on March 16, 2022, the portfolio has declined by $1,698.6 billion or right on $1.7 billion.

The Reserve Balances with Federal Reserve banks, a proxy for the excess reserve in the banking system, has declined by $624.5 billion.

The Fed liability account that has declined to offset the decline in the securities portfolio has been the line item for Reverse Repurchase Agreements, which has declined by $984.4 billion.

Rounding off, on the asset side, the securities portfolio has declined by $1.7 trillion. On the liability side, the account for Reverse Repurchase Agreements has fallen by about $1.0 trillion. The residual, the account for Reserve Balances with Federal Reserve Banks has fallen by $0.6 billion.

These are the primary Federal Reserve accounts that have played a role in the quantitative tightening program that the Federal Reserve has been on since March 16, 2022.

The commercial banking system is still sitting on a lot of cash.

The total amount of Reserve Balances with Federal Reserve Banks was $3,268.9 billion on June 26, 2024, or almost $3.3 trillion.

Looking at the amount of cash on hand, reported on the Federal Reserve’s H.8 statistical release, “Assets and Liabilities of Commercial Banks in the U.S.” we find the total cash on bank balance sheets to come out a little over $3.4 trillion

So the commercial banking system, as a whole, has lots and lots of cash around.

This speaks to one of the major problems facing Federal Reserve leaders these days. How did so much money get into the banking system and how is it impacting relevant monetary variables?

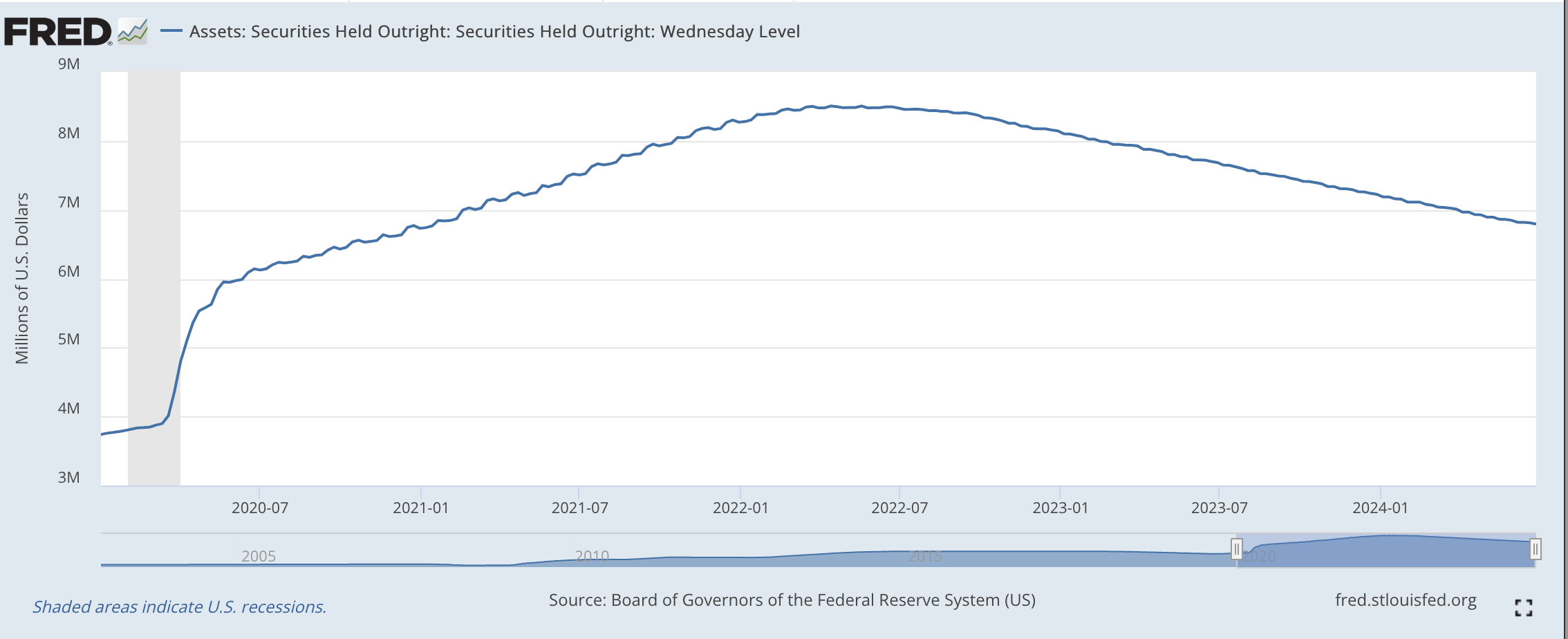

Well, here is a picture of the securities portfolio going back to early March 2020, near the mid-point of the last recession.

Securities Held Outright (Federal Reserve)

{kind=link}

The amount of securities held by the Federal Reserve on March 4, 2020, was just under $3.9 trillion.

You can see how the Fed responded to the Covid-19 pandemic and to the subsequent recession. The Federal Reserve bought securities!

On March 16, 2022, the day the Federal Reserve began its program of quantitative tightening, the securities portfolio peaked-out at $8.5 trillion. So in two years time, the Federal Reserve added $4.6 trillion to its securities portfolio.

As described above, since March 16, 2022, up to the latest banking week, the Federal Reserve has reduced its securities portfolio by $1.7 trillion.

But, overall, since March 4, 2020, the Federal Reserve has seen its securities portfolio increase by 74.4 percent.

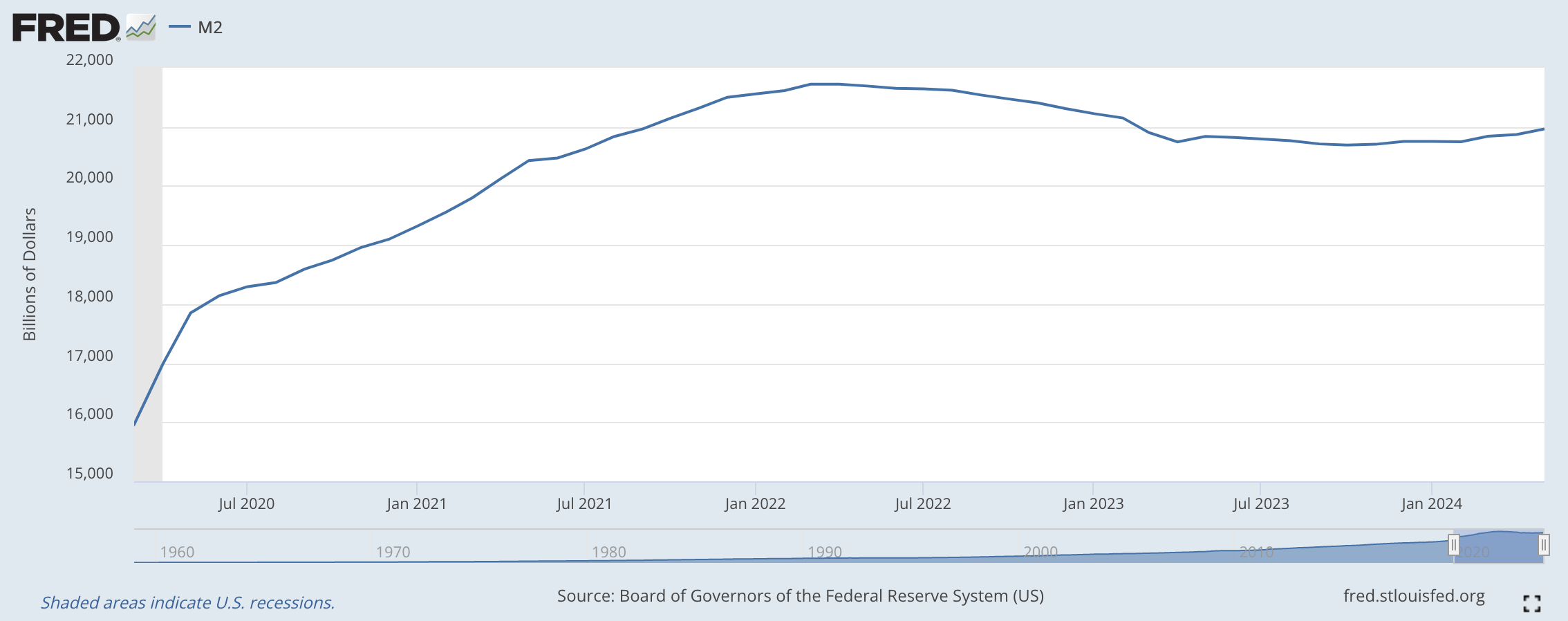

And, how has this impacted the M2 money stock?

M2 Money Stock (Federal Reserve)

{kind=link}

In March of 2020, the M2 money stock was right around $16.0 trillion.

At its peak in March of 2022, the M2 money stock was just over $21.7 trillion.

And, now in June of 2024, the M2 money stock is down to about $21.0 trillion

So, over the past four years or so, the performance of the M2 money stock pretty well duplicates what we saw happen to the Fed’s securities portfolio.

Now analysts and investors have been worried about the decline in the M2 money stock over the past 16 months or so.

Do they have a real cause for concern?

My answer to that question is “no,” they do not have a real concern because, starting from March 2020, the securities portfolio of the Fed has risen by almost $3.0 trillion.

And, over the same time period, the M2 money stock has risen by $5.0 trillion.

Furthermore, the “excess reserves” in the banking system have risen from $1.7 trillion in early March 2020 to $3.4 trillion currently.

Commercial banks are carrying far more cash assets on their balance sheets than they have ever done before.

The real question is not about the “tightening” of the “quantitative tightening” program, but about all the cash left in the banking system that was forced into the banking system as the Federal Reserve fought to “err on the side of monetary ease” when it was fighting the spread of the Covid-19 pandemic and subsequent recession.

The growth of the M2 money stock turned negative as the Fed began its quantitative tightening but has lately flattened out.

But, as can be seen in the chart above, the M2 money stock is still way above the level it began at in 2020.

Conclusion: there is plenty of money around in the banking system.