Federal Reserve: Auto loan balances increase by $11 billion in Q4

By

on February 21, 2025

Announcements | Market Trends

Household debt increased by $93 million, reaching $18.4 trillion, while auto loan balances increased by $11 billion to $1.66 trillion during Q4 2024, according to the Federal Reserve Bank of New York.

Yahoo Finance reports $18.4 trillion is a new high caused mostly by inflating credit card balances that increased by about 4% to a record $1.21 trillion.

A more concerning trajectory is the serious delinquency rates, especially for auto loans and credit cards, the article says.

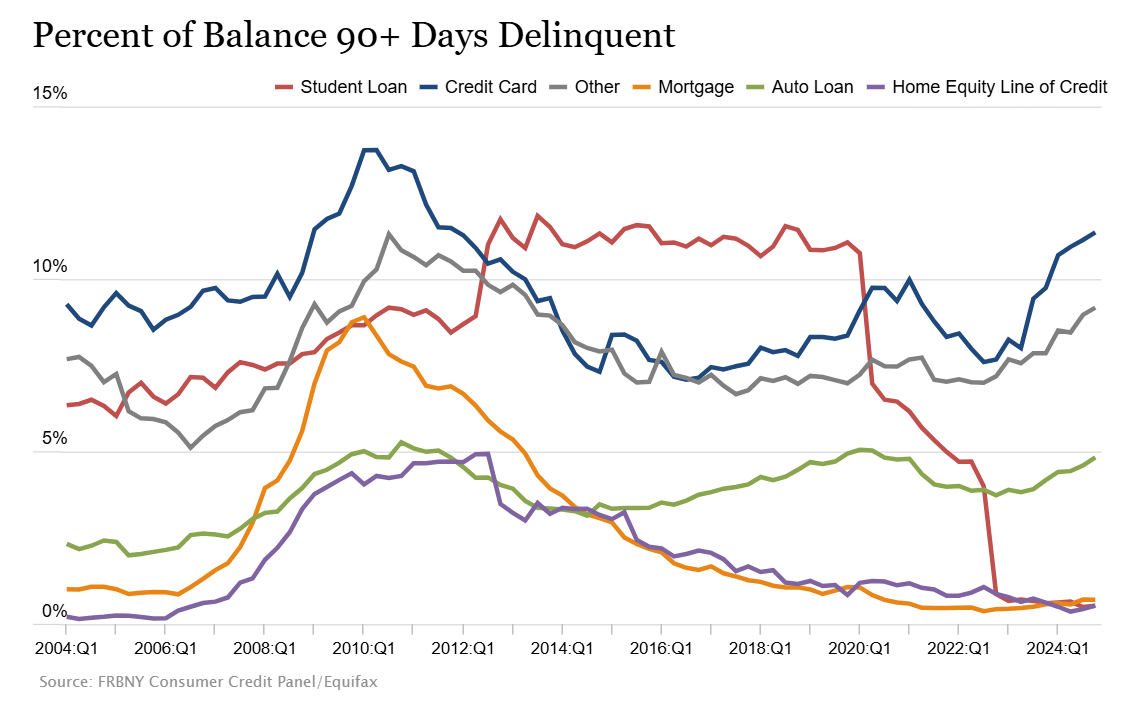

According to the Federal Reserve, 4.8% of auto loans were 90 days or more delinquent in Q4. This was up from 4.2% in Q4 2023. Credit card delinquency of 90 days or more was 11.4% in Q4.

{kind=link}

“I really see a trend of automobile loan payments being very high and causing a lot of stress on how people pay for living expenses and [their] increasing reliance on credit,” Victor Russell, operations manager for nonprofit credit counseling agency Apprisen, told Yahoo Finance.

Traditionally, households start digging out of debt at the start of a new year, Yahoo Finance says.

“But that decades-long trend may be disappearing, not because borrowers are out of their debt stranglehold but because they now need help throughout the year for their pricey car loans and ballooning card debt,” Yahoo Finance says.

Russell told Yahoo Finance that, typically, a car payment should take up no more than 13-14% of an individual’s net income but currently, individuals are using 21-22% of their income toward car payments.

“That’s almost a quarter of your income just servicing an automobile loan payment,” Russell said in the article. “That’s not sustainable.”

Russell also said that the term lengths on the loans have increased to 78 months when they used to be 48-60 months long.

The article says some car owners have turned to credit cards, averaging about 20%, to help pay expenses.

CCC Top 2024 Trends Report said the average transaction price was $48,623 in October while the average new vehicle financing rates have been 7% higher for the past two years.

About 17% of new auto loans have monthly payments of $1,000 or more, down slightly from 17.9% in Q4 2023. However, as of Q3 2024, 24.2% of new vehicle sales with a trade-in had negative equity with consumers upside down in their auto loans, owing an average of $6,548.

Higher payments could result in consumers keeping their vehicles longer. As of 2024, 66% of vehicles in operation are seven years or older and the average U.S. vehicle age has now increased to 12.6 years.

The report notes that the aging car parc could also mean consumers with older vehicles are more prone to increase deductibles or drop first-party coverages, decreasing policy limits. The consumer also could elect to go without insurance altogether.

IMAGES

Photo courtesy of atakan/iStock

Graph courtesy of Federal Reserve

Share This:

Related