Mercedes-Benz: >10% Potential Yield Supports Bullish Case For Share Price Rebound

franz12

Mercedes-Benz Group AG (OTCPK:MBGAF) (OTCPK:MBGYY) has disappointed investors YTD, as Q1 under-performed expectations and uncertainty surrounding the impact of a potential tariff-war between the EU and China pressured investor sentiment. However, underneath the uncertainty and temporary weakness in earnings momentum, investors should appreciate that Mercedes-Benz continues to stand out as a resilient and well-managed premium/luxury car manufacturer, well-positioned for a significant commercial rebound in the second half of 2024. The China tariff narrative will likely turn out less negative than feared, and the earnings challenges encountered in early 2024 are being effectively addressed through strategic initiatives aimed at enhancing supply chain efficiency and resolving production bottlenecks. Overall, Mercedes-Benz continues to demonstrate strong structural earnings capability with an EBIT margin between 10-12%, which is anticipated to provide capital returns to equity investors significantly exceeding the double-digit benchmark. Using a valuation based on a residual earnings model, I uphold my “Strong Buy” rating for MBGAF, setting the target price at $147 per share.

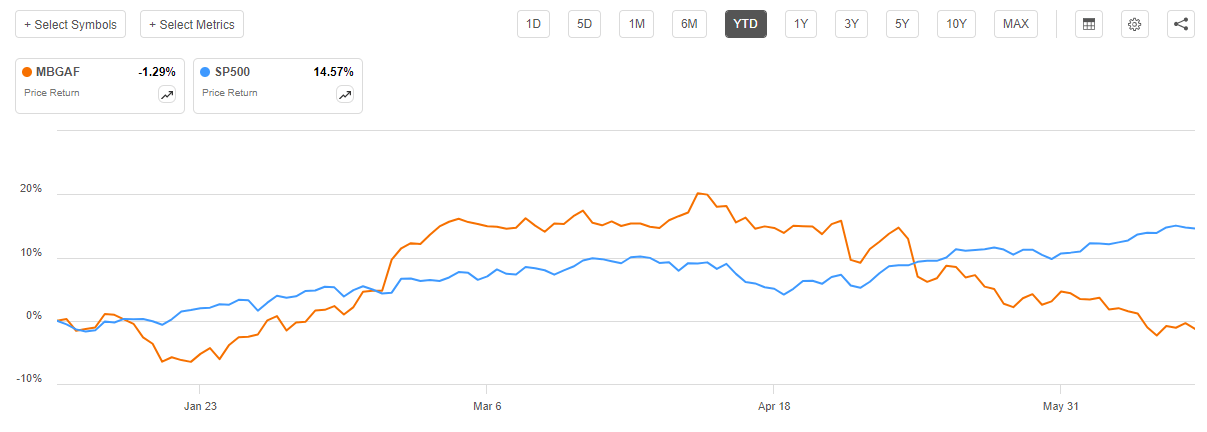

For context: Mercedes-Benz stock has significantly under-performed the broader equities market this year. Since the beginning of the year, MB shares are down approximately 1%, compared to a gain of about 15% for the S&P 500 (SP500).

{kind=link}

The Elephant In The Room: China Exposure

Mercedes-Benz stands out as the second most exposed European OEM to the Chinese market, with about 35% of its unit sales originating there. On that note, it is not surprising that Mercedes-Benz shares have suffered from the lingering uncertainty surrounding a potential car/ automotive tariff war between the European Union and the Chinese Chamber of Commerce. MBGAF stock lost about 10% of market cap since speculations on potential tariffs heated up in April this year. However, the financial impact on Mercedes-Benz, as a consequence of the tariffs and based on the current situation, may be much less severe than initially feared. According to a research note by UBS, based on a meeting with Mercedes-Benz CFO Harald Wilhelm, the financial impact of retaliatory tariffs should likely be limited, and manageable as Mercedes-Benz is considering increasing localization efforts, which could include ramping up local production of models like the GLE:

Should there be retaliation by China on a potential EU tariff announcement this week (the Chinese Chamber of Commerce recently warned to the EU about a potential 25% tariff on ICE cars with larger engines >2.5 liter; link), he thinks that over time, there could be more localization by Mercedes. He said that out of Mercedes’ c150-200k annual imports into China, only about half have an engine size >2.5 liter so that only the highest-mix vehicles would be potentially affected.

(Source: UBS research note on Mercedes-Benz, dated June 10th: Mercedes-Benz Group AG Feedback from CFO roadshow).

On a broader perspective, it is worth noting that Mercedes-Benz’ sales in China have consistently outperformed the broader market, benefiting from the clear distinction between the luxury and mass-market segments. As a luxury consumer product, Mercedes-Benz cars should be less affected by tariffs compared to more price-sensitive cars like those sold by Volkswagen.

Setback In Financial Performance Should Prove Temporary

Mercedes-Benz’s Q1 2024 performance highlighted several challenges, including a decline in car margins to 9% from 14.8% in Q1 2023. This decrease was primarily due to supply chain disruptions and model changeovers in top-end vehicles like the G-Class, AMG E-Class, and GLC. Additionally, 48-volt supply issues impacted core models such as the E-Class, resulting in an 8% YoY decline in overall car volumes. However, these issues are expected to be temporary. In the earnings call with analysts, and on roadshows with investors, management has voiced strong confidence in resolving these bottlenecks as the year progresses. The anticipated improvements in supply chain dynamics and the resolution of the 48-volt issues by Q2 2024 are set to restore production efficiency and support margin recovery. Importantly, despite these challenges, Mercedes-Benz managed to maintain its revenue per unit (excluding China) at a positive growth rate of 0.5% YoY. On top of the stable revenue outlook, and despite the soft performance in Q1 2024, Mercedes-Benz has maintained its full-year guidance for earnings, projecting a car EBIT margin of 10-12%. Additionally, the company aims to reach net-zero working capital by the end of the year, which should further enhance its financial position and support a solid case for enormous capital distribution.

Equity Yield Likely To Push >10% Over The Next 12 Months

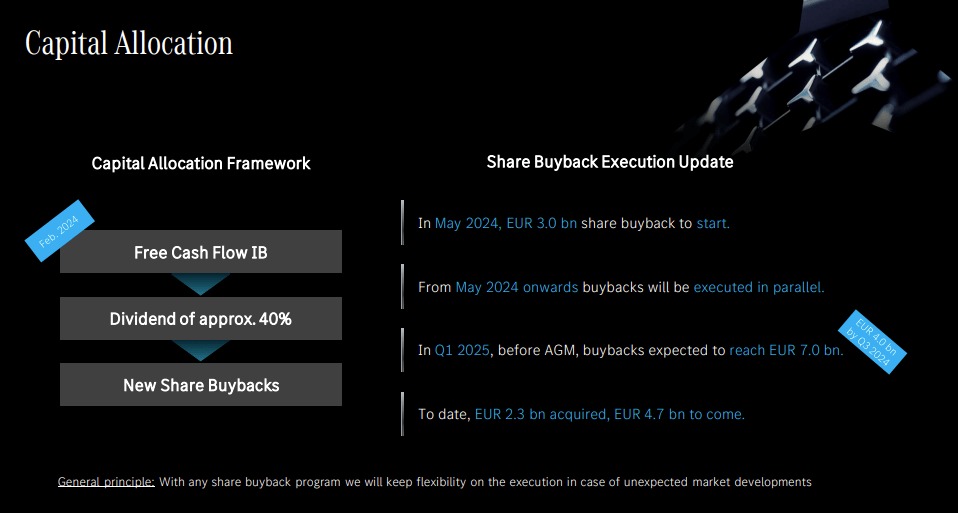

One of the most compelling aspects of Mercedes-Benz’s investment case is its strong capital return program. The company has committed to a shareholder-friendly capital allocation strategy, including a significant dividend payout and aggressive share buyback programs. Specifically, in 2024 Mercedes-Benz management plans to pay out approximately 40% of its industrial free cash flow in form of dividends, which should amount to about €4-5 billion. And on top of this, management has suggested that by Q1 2025, the company is planning to repurchase €7 billion worth of shares, of which €4.7 billion are still outstanding. Notably, The buyback program alone represents approximately 8.75% of the company’s market capitalization. Including the dividends, the shareholder return pushes well beyond the double-digit yield benchmark. Needless to say, this robust capital return strategy should positively reflect on the company’s confidence in its financial stability and future earnings potential.

Mercedes-Benz Investor Roadshow

{kind=link}

Valuation Update: Raise TP To $147/Share

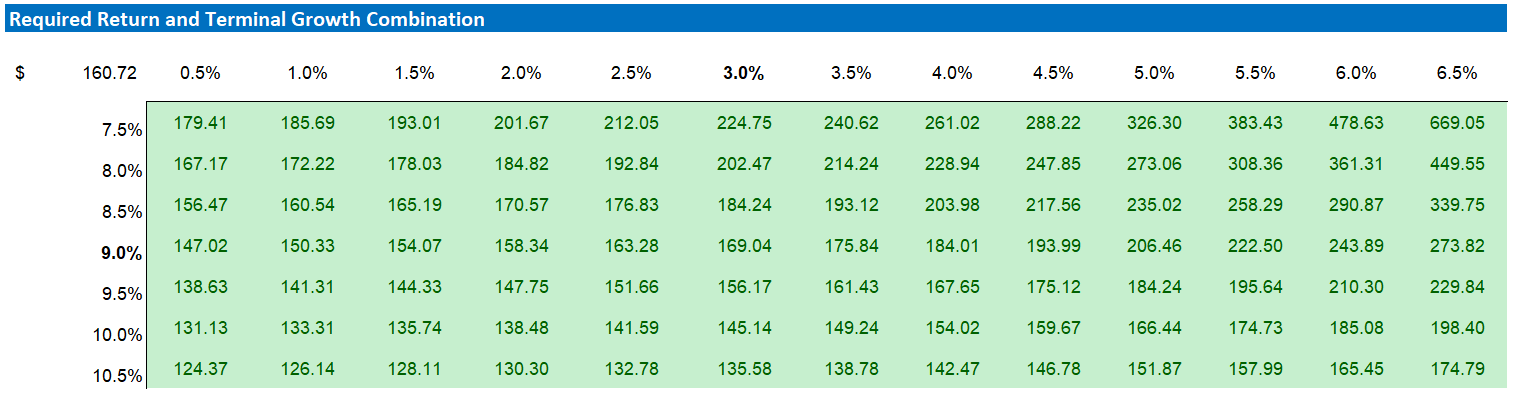

Aligning my earnings estimates for Mercedes-Benz with the latest industry trends and financial reports, I am revising my valuation assumptions for the company’s stock. Based on analyst consensus estimates, with adjustments of +/- 10%, I now project Mercedes-Benz’s earnings per share for FY 2024 to range between $11.9 and $12.2. Additionally, I forecast these earnings will rise to $13.3 in FY 2025 and $13.5 in FY 2026. Beyond FY 2026, I anticipate a compound annual growth rate in earnings of approximately 2.25%, which is about in line with projected nominal GDP growth and likely conservative. At the same time, I am lowering my cost of equity assumption by 25 basis points, to 9%, mostly as a reflection of a softening interest rate environment. With these updates, I now assess the fair value of Mercedes-Benz stock at $147, which is well below Mercedes-Benz’s current market trading price.

For context, the value “Speculation” is just the difference to fair implied value. A positive value implies a premium; or in other words, markets are speculating to price more fundamental upside compared to my estimates.

Company Financials; Bloomberg & Author’s EPS Estimates; Author’s Calculation

Below also the updated sensitivity table.

Company Financials; Bloomberg & Author’s EPS Estimates; Author’s Calculation

{kind=link}

Investor Takeaway

Mercedes-Benz Group AG stands out as a resilient and well-managed premium/luxury car company, poised for an improving commercial rebound towards the second half of 2024. The temporary challenges faced in early 2024 are being addressed with strategic initiatives aimed at improving supply chain efficiency and resolving production bottlenecks. On that note, the company’s strong earnings power, with 10-12% EBIT margin, should enable capital returns for equity investors well above the double-digit benchmark. As a function of valuation anchored on a residual earnings model, I maintain my “Strong Buy” rating for MBGAF with a $147 per share target price.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.