Understanding the methodology behind Moody’s US downgrade

Stay informed with free updates

Simply sign up to the US economy myFT Digest — delivered directly to your inbox.

Even if it’s no longer deserving of a Aaa rating, Aa1 is a really strong rating for a fiscal basket case. How does Moody’s get there for the US government?

Moody’s, just like the other rating agencies, is generous in providing transparency to their rating methodologies. In their Sovereign Rating Methodology document, the rating agency lays out the thinking that guides consistency in overall ratings.

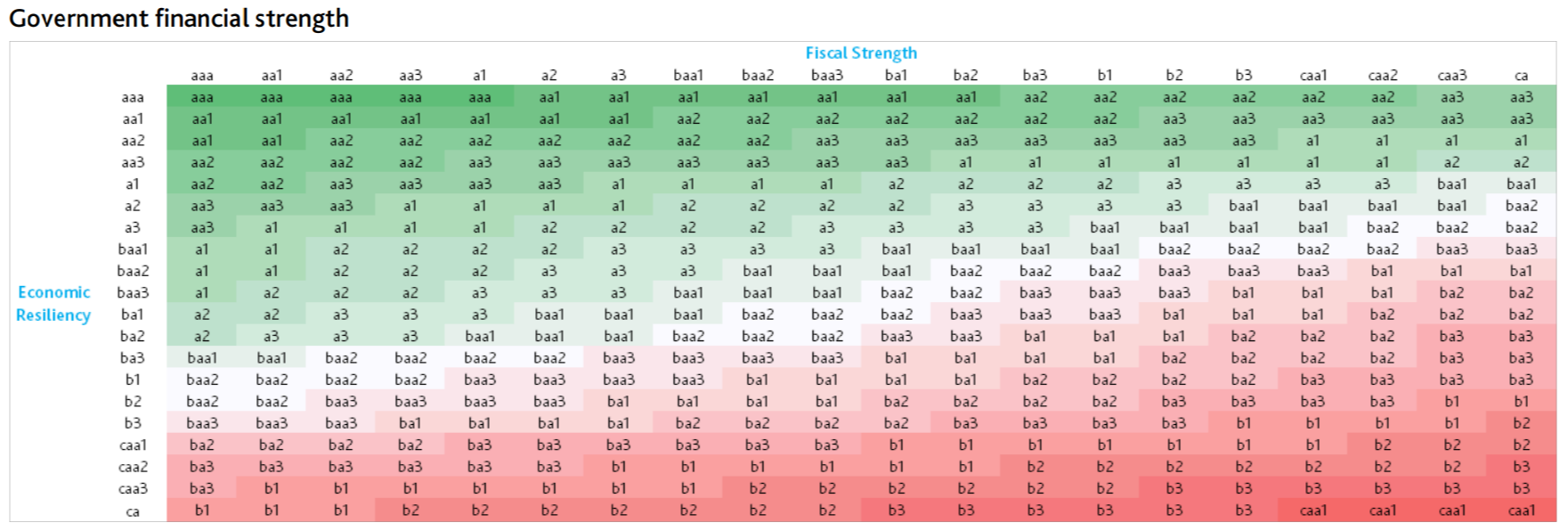

Rather than focusing on just one bunch of fiscal metrics, Moody’s outlines a vast series of criteria and benchmarks that they then wrap into their ‘Economic Resiliency’, ‘Fiscal Strength’, and ‘Susceptibility to Event Risk’ factor ratings. The Economic Resiliency and Fiscal Strength factors then mesh together to produce an overall Government Financial Strength rating, like so:

{kind=link}

We know that Moody’s Economic Resiliency factor rating is ‘aa1’ for the United States because the firm tells us in its rating opinion. Frankly, the Economic Resiliency score is the one that the US should be absolutely crushing.

Massive economy? Check. High GDP per capita? Check. High-quality legislative and executive institutions, strong civil society institutions, and independent judiciary? Okay, so maybe there are some chinks in the armour.

Still, ‘aa1’ is a really very good rating.

Readers will note from the table above that, given an Economic Resiliency factor rating of ‘aa1’, the Fiscal Strength factor rating must be at least ‘a3’ to to achieve an overall ‘aa1’ Government financial strength sub-rating.

Does the US have a Fiscal Strength factor rating of at least ‘a3’? We find it hard to see how.

What goes into the Fiscal Strength factor rating? Some numbers and some judgments.

On the numbers side, there’s a scorecard that we’ve reproduced below.

Note: Moody’s forecasts general government debt/ GDP and general government interest payments/ revenue. We’ve translated these into debt/ revenue and interest/ GDP metrics using the CBO’s 2035 forecast for revenues as a percentage of GDP.

For most sovereigns, the two debt burden metrics and the two debt affordability metrics are equally weighted. But because the US is a reserve currency issuer, Moody’s tweaks the weights on its scorecard so that the Debt Burden sub-factors each attract a 5 per cent weight, and each Debt Affordability sub-factor attracts a 45 per cent weight.

Where does this leave us? Using the CBO’s numbers for 2025 we reckon the United States’ raw Fiscal Strength factor rating comes out at maybe ‘ba3’. And using CBO 2035 forecasts, it looks like it will fall to ‘b2’. But using Moody’s forecasts, we calculate this factor rating slips all the way down to ‘caa2’.

Gulp.

Regardless of whether we should be looking at the 2025 numbers or Moody’s 2035 projections as inputs, these scores are a long way below the ‘a3’ Fiscal Strength factor score consistent with an Aa1 rating.

True, Moody’s does adjust the raw output. It can lower the score by as much as two notches if debt is trending higher (although this shouldn’t affect the US, as its debt trends slide just below the radar). It can also adjust the score up or down depending on an expectations element. And there are a bunch of other adjustments (like how much foreign currency government debt there is, or the size of government’s financial holdings are). These adjustments can collectively shift the Fiscal strength factor up to six notches.

After going through the methodology, we reckon there could be one notch taken off to reflect expectations. But we don’t immediately see any other factors that would move the needle.

However, Moody’s can move a further three notches based on our favourite metric — ‘Other’.

Moody’s doesn’t reveal where it ends up on the standalone Fiscal Strength factor score for the United States. But we can easily see how the answer could be somewhere in the ‘ba1’ to ‘caa1’ range.

Again, these scores are a long way below the ‘a3’ Fiscal Strength factor score consistent with a Aa1 rating. And if the rating process was entirely programmatic, the highest ratings we would expect are Aa2 or Aa3.

So what have we learned?

First, despite being an extremely large, rich and dynamic economy, the US is — from a credit rating agency perspective — moving into fiscal basket case territory. But perhaps surprisingly, no matter how bad the fiscal metrics look, it will be hard for America to slip lower than an Aa3 Moody’s rating without more general economic resiliency starting to crack, or some susceptibility to event risk creeping in.

Second, while metrics and scoreboards can be nice ways to break down rating vulnerabilities and areas of strength, any scorecard is going to provide a rough guide at best. Sovereign Issuer Ratings emanate from committees of humans who bring judgment and accountability. And this is a good thing.