Federal Reserve Watch: Banking System Doing OK

drnadig

Let’s look at what the Federal Reserve did over the past year concerning handling the “excess reserves” of the commercial banking system.

The account on the Federal Reserve’s balance sheet, the H.4.1 release, shows a line item entitled “Reserve Balances With Commercial Banks.”

I have often referred to this account as the excess reserves of the banking system, an account that provides us with some information on the monetary position of the Federal Reserve.

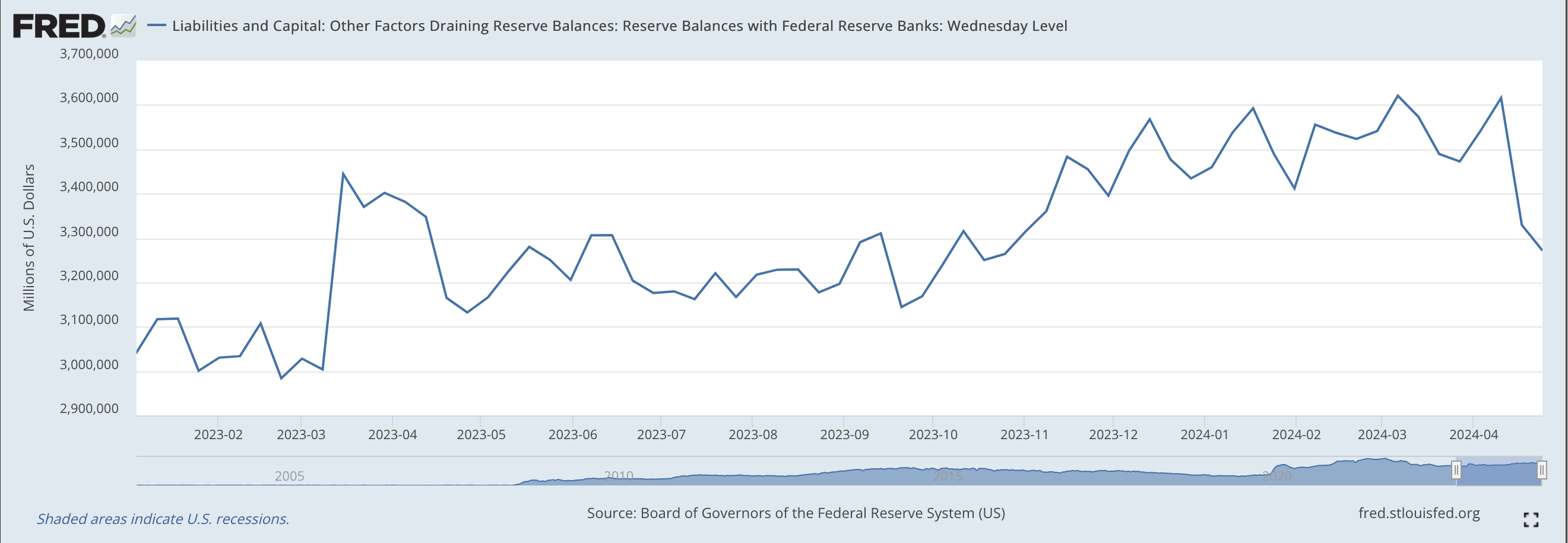

Here is the chart showing the data from early March 2023.

Reserve Balances with Federal Reserve Banks (Federal Reserve)

{kind=link}

Given the direction of this chart, it appears as if, for the last 12 months or so, the Federal Reserve has been overseeing the RISE in excess reserves in the banking system.

One can see from the “big jump” in reserve balances in March 2023 the response of the Federal Reserve to the disruptions happening in the commercial banks as a couple of large commercial banks failed at that time.

But, for a good portion of the last year, excess reserves have been increasing in the commercial banking system.

And, almost all the way through this specific time period, the Federal Reserve has been dealing with the issue of when it will begin to reduce its policy rate of interest.

Meanwhile, the Federal Reserve continues to reduce the size of its securities portfolio.

And, note, that the amount of excess reserves that are held by the commercial banking system totals just under $3.3 trillion!

There is plenty of cash in the banking system.

What is it that is supplying this “cash” to the banking system?

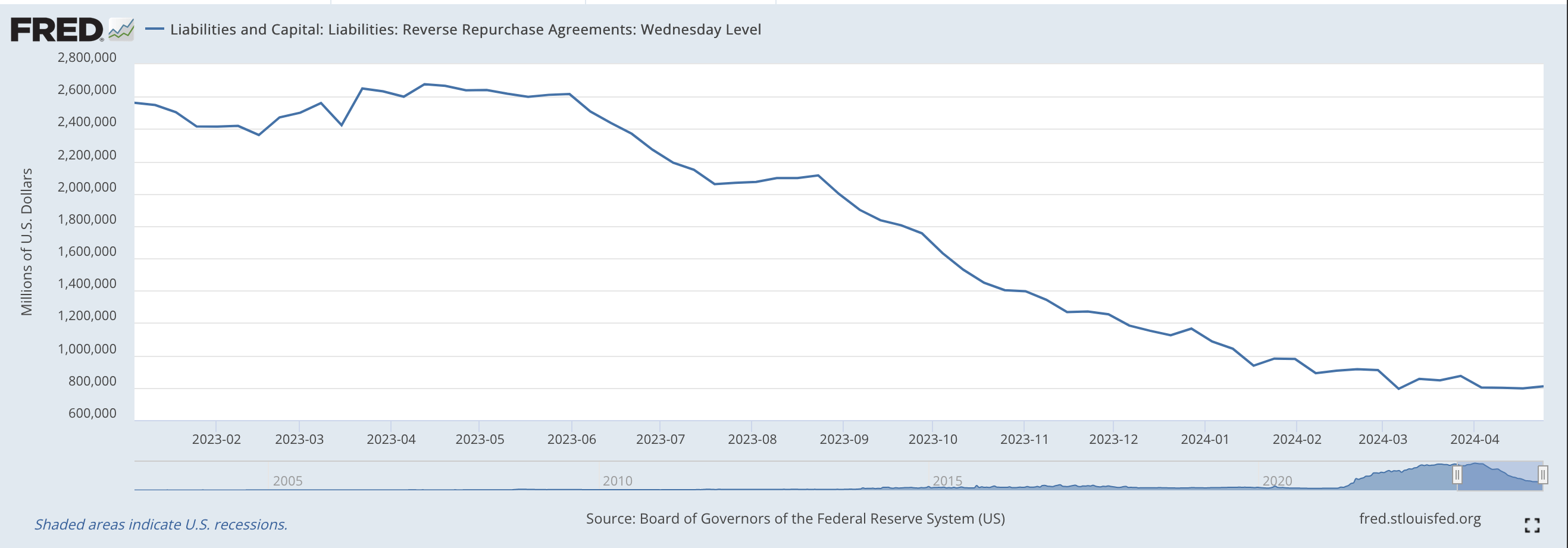

Well, surprise, surprise. The primary supplier of these reserves to the banking system has been the reduction of commercial bank use of the reverse repurchase agreement window.

Reverse Repurchase agreements (Federal Reserve)

{kind=link}

That is, commercial banks, themselves, have been using this window less and less frequently.

Thus, the excess reserves of the banking system have increased as cash flows back into the banking system.

Over the past year, the Federal Reserve has continued to let securities leave its securities portfolio and looked on as the Reverse repos used by the banking system have declined.

The banking system has been sufficiently liquid all through the decline in the Fed’s securities portfolio.

Conclusion: the Federal Reserve has steadily maintained its securities portfolio reduction, but, at the same time allowed a “fluid” use of the reverse repurchase agreement window to help the banking system stay liquid.

As a consequence, most commercial banks, especially the larger ones, appear to be more than comfortable with the amount of “cash” they have on hand.

If we look at the Federal Reserve H.8 release, concerning commercial banking data, we see that on April 10, 2024, the largest, domestically chartered commercial banks hold a not seasonally adjusted amount of cash that totals over $1.8 trillion. This is the largest 25 domestically chartered banks in the U.S.

All commercial banks in the H.8 release hold just $3.6 trillion in cash assets.

Thus, 25 commercial banks in the U.S. hold one-half of the cash assets of the country. There are over 4,000 commercial banks in the U.S. that hold the other half.

The largest commercial banks in the U.S. seem to be in pretty good shape. And, for all we can tell, these banks have been putting aside a lot of cash to prepare for possible loan losses.

Especially encouraging to me is the fact that Reserve Balances with Federal Reserve Banks…the proxy for excess reserves…has been going up as the use of the Fed’s reverse repurchase agreement window has been in major decline.

One could argue that the Fed’s methodology used to reduce the size of its securities portfolio has worked quite well.

Still remaining, however, is the fact that the Fed still holds $6.9 trillion in securities portfolio. The Fed has reduced the size of its securities portfolio by almost $1.6 trillion since it began its quantitative tightening program.

With commercial banks still holding $3.6 trillion in “cash”, one can still worry about how the Federal Reserve is going to continue to reduce the size of this holding.

Banks holding $3.6 trillion in “cash” is not “normal.”

One could say that the banking system was still in disequilibrium as a result of what took place during the fight against the Covid-19 pandemic.

But, the Fed has been able to get us this far.

Hopefully, it will be able to successfully manage us the rest of the way back to a “more normal” environment.

As far as the Fed lowering its policy rate of interest, I think the Fed is going to go slow on this. One major reason holding the Fed back is the value of the U.S. dollar and the fact that other countries are not lowering their policy rates that quickly.

I think the Fed wants to keep the value of the U.S. dollar strong, and to cut its policy rate of interest too quickly would not help it accomplish this goal.

I believe that as long as the financial markets remain pretty stable, I think the Fed will take its time to reduce its policy rate. Given the continued strength of the U.S. economy and the failure of inflation to come down further, the Fed will not have sufficient justification to lower its rate.

A relatively strong U.S. economy is the foundation for the narrative of the rest of 2024.

cha