Moderately Bullish On 2024: Markets To Overcome Pessimism And Challenges

We Are

Introduction

Projecting what the markets may do for the remainder of calendar year 2024 is the main purpose of this article. This is a challenging task given all the factors that drive markets, economies and investor (and trader) habits and behaviors.

Most investors pay fairly close attention to their portfolios. This may be for better and for worse. Investors also may trade portions of their portfolios, which adds to any interest in the relatively short term. Others are market aficionados and enjoy tracking economic and market trends.

2024 Q1 Performance

The markets have had an excellent start to 2024, as illustrated by this chart:

{kind=link}

Overall market performance in Q1 has also been solid, as shown in this chart from Nixon Peabody. The S&P and the Nasdaq have led the way, but it’s noteworthy that the MSCI All Country World Index also is clearly positive.

If this performance were to continue for the remaining three quarters of 2024, it would be a spectacular year. The first two weeks of April suggest the markets are in at least a mild short-term correction – but not more.

Here’s another view of key takeaways from Q1:

- U.S. GDP grew at 3.2% in Q4 2023 while February’s annual inflation reading rose to 3.2%. The Atlanta Fed forecasts Q1 2024 GDP at 2.3%.

- Expectations for Federal Reserve (Fed) rate cuts have declined due to stickier-than-anticipated inflation.

- U.S. stocks returned an impressive 10.6%, while U.S. bonds fell by 0.8%. The MSCI ACWI ex-U.S. Index was up 4.3%.

- Major stock market indexes have been dominated by a select few mega-cap technology companies.

- Recessions are occurring in Japan, the U.K., Finland and Ireland, and negative GDP rates for Q4 2023 were also reported in Germany and Canada.

The bullish performance of megacap technology companies is often seen as a distortion destined to derail markets. I think the “Magnificent Seven” are a reflection of the technological revolution that’s a positive and secular trend.

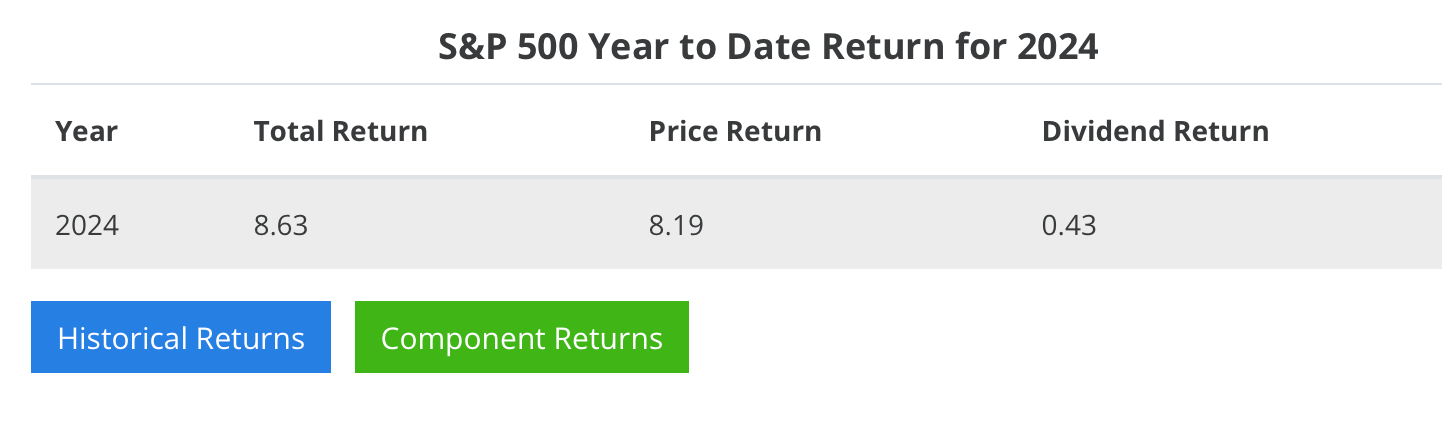

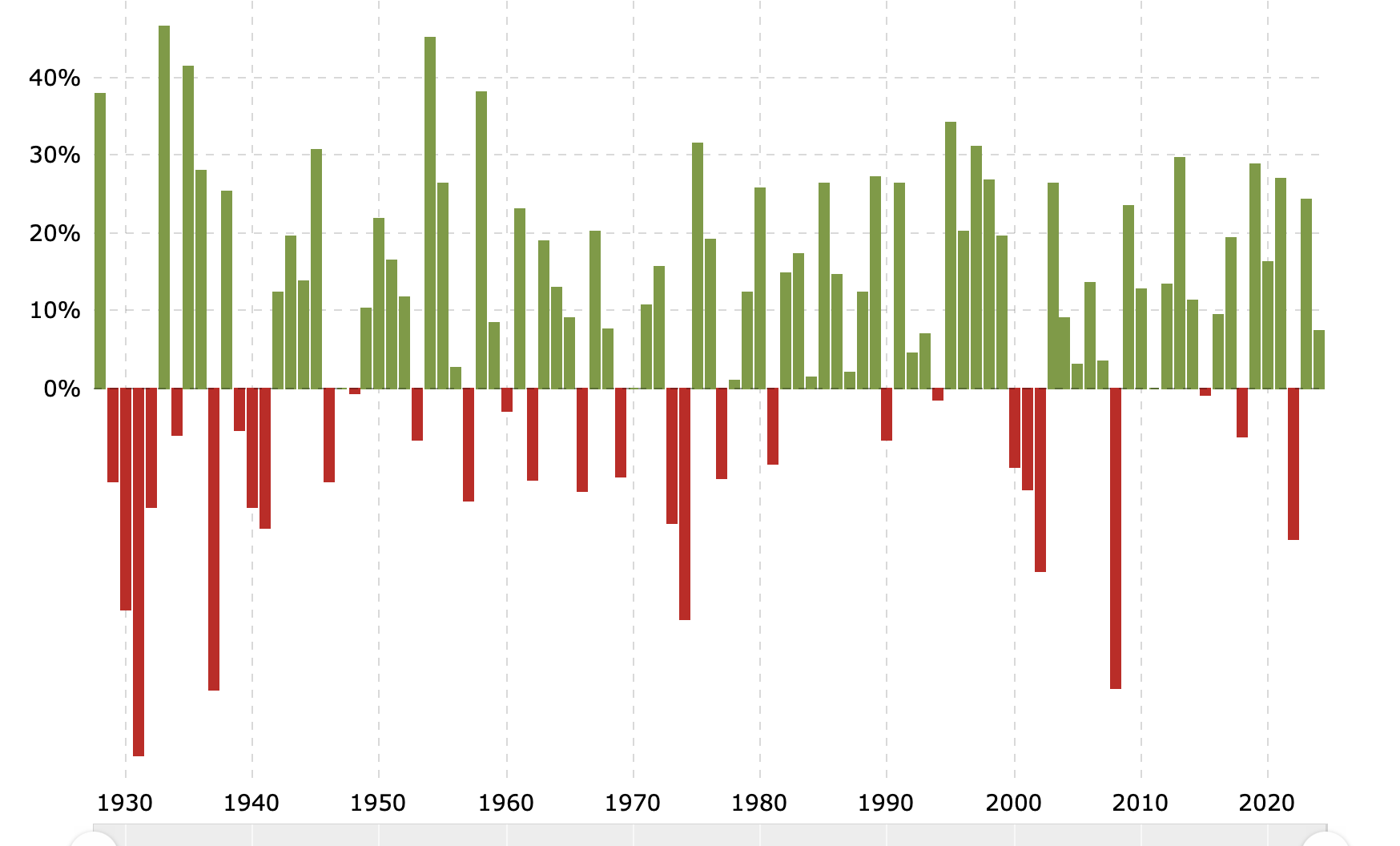

This is a view of historical returns for the S&P average:

{kind=link}

2024 to date is the small vertical green bar on the far right. Quadrupling its 8.63% return would result in a solid year – but still below the very best years.

Counter Indicators

Some famous indicators suggest that markets may be generally overvalued and future returns limited. For instance, the Buffett Indicator is broadcasting caution. This compares total market cap vs. the US Gross Domestic Product (GDP). The ratio is currently at 185%, which leads to a statistical expectation of returns of 0.5% per year, including dividends, if past market performance relative to the indicator is the basis for evaluation.

Add the assets of the Federal Reserve Bank to the GDP and compare total market cap to the GDP plus Fed assets, and the Buffett number is 146%. Even with this slight ratio improvement, expected returns are estimated at 1.1%.

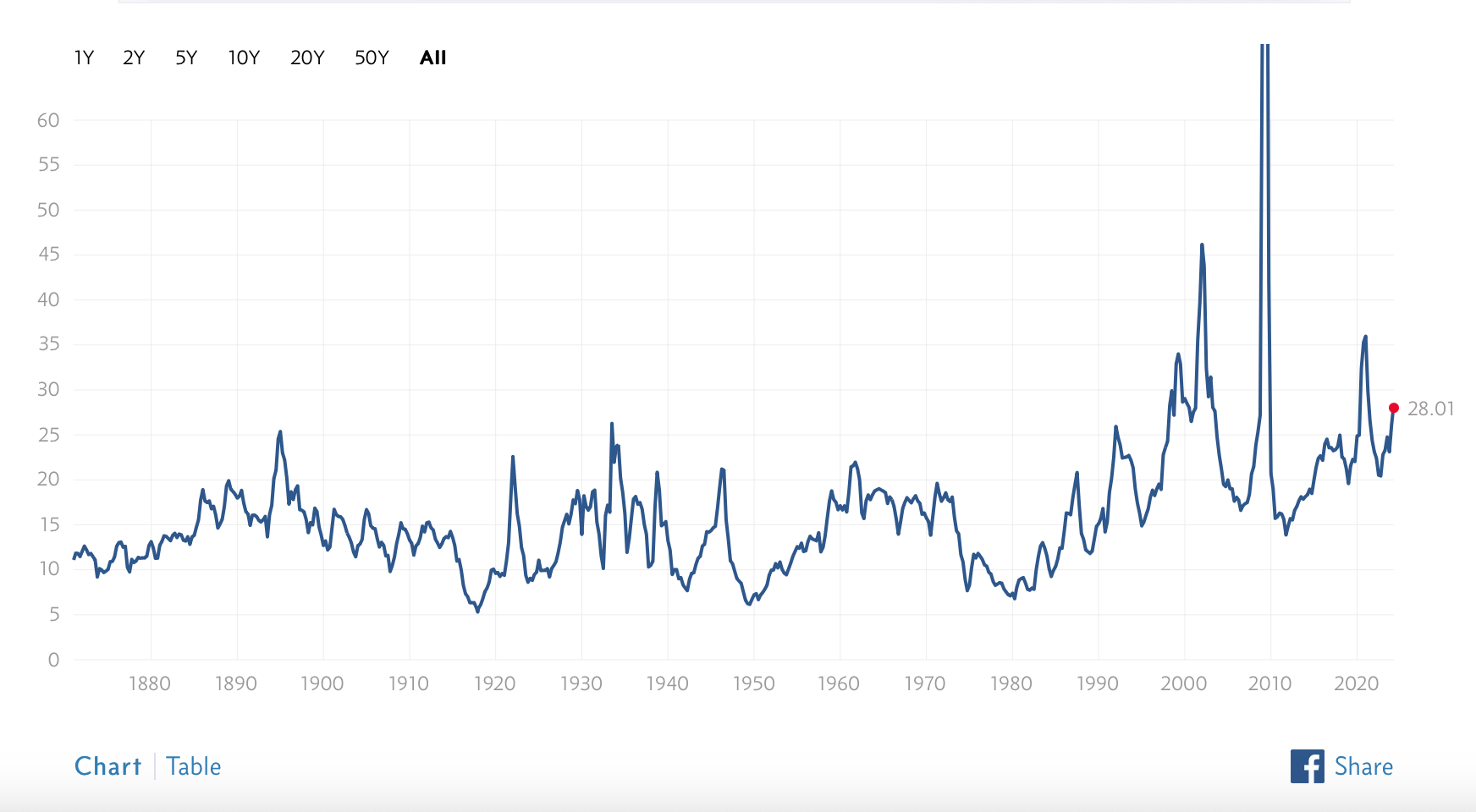

If we consider overall market price to earnings ratio and compare that to historical figures (again using the S&P as a benchmark), we arrive at 28:

{kind=link}

Another reading is 27.07, this from GuruFocus.

This is admittedly higher than the smoothed average for the S&P, which states the median value (historically) as 17.89. Without a doubt, 27-28 is a good bit higher than a historical figure just under 18. Others claim the actual PE ratio is lower than 27, or “subtract” the higher PE numbers for the Magnificent Seven (megacap tech companies) to arrive at a lower number for the great majority of publicly traded companies.

Could there be legitimate reasons for the collective PE rising over time? Part of the answer lies in whether the technological advancements driving new efficiencies are also agents of deflation.

The State of Economies and Markets

There’s much negative commentary about the state of both economies – including the U.S. economy – and the markets. This view is based on the intersection of negative developments in the areas of inflation, employment government fiscal and Federal Reserve monetary policy. The pessimism also factors in issues from consumer debt to market valuations to geopolitical risks.

At the same time, investors require a certain optimism that the stock market remains the best option for building personal financial security. A strategic bearishness does not fit a strategy of building wealth through market investment. Still, if the facts fit a bearish framework, an honest investor might reexamine a financial strategy that revolves around securities.

My own market’s base case is a tempered version of that of a Deloitte analyst called Robyn Gibbard, who created a forecast for Q1 of 2024:

“The US economy continues to surprise to the upside. Despite persistent fears around high-interest rates, high inflation, slowing growth, and unsustainable consumer spending, the economy continues to deliver month after month. It is looking increasingly as though policymakers have managed to create the conditions for the mythical ‘soft landing,’ where inflation is brought down to target without causing a recession.”

“Deloitte’s baseline forecast remains optimistic, and we expect the US economy to continue to perform well in the short-term thanks to strength in the job market, consumer spending, and exports…”

If we include March inflation statistics (see below) and accept that the Federal Reserve may reduce its own projection of three interest rate cuts for 2024, then tempering Gibbard’s optimism somewhat makes sense.

Inflation and Fed Policy

Inflation in the United States persists. The Federal Reserve’s inflation target of 2% per year is clearly at risk.

Seeking Alpha described the March inflation statistics:

“The Consumer Price Index climbed 0.4% in March, the same increase as in February, and exceeding the 0.3% rise that economists expected… the hot readings in January and February may be more than a “bump” on the path to inflation heading toward the Federal Reserve’s 2% goal… the indexes for shelter and gasoline both increased in March, contributing more than half of the monthly increase in the all-items index. The energy index jumped 1.1% over the month, and the food index edged up 0.1%.”

“On a year-over-year basis, March’s CPI climbed 3.5%, in line with expectations and accelerating from 3.2% in the prior month.”

“…’We have a strong economy, with tight inventories and pricing power for companies,’ said David Russell, global head of Market Strategy at TradeStation. ‘That’s now turning into a double-edged sword, making inflation stickier than we hoped. Rate cuts could be out the window.'”

There was better news on the Producer Price Index:

“The Producer Price Index rose 0.2% in March, less than the +0.3% expected and slower than the +0.6% pace in February, the U.S. Department of Labor said on Thursday.”

“Core PPI, which excludes food and energy, also increased 0.2% M/M vs. +0.2% expected and +0.3% prior. Compared with a year ago, core PPI rose 2.4%, topping the 2.3% expected and accelerating from the 2.0% pace in February.”

“‘PPI a little more calm than CPI in March, but story similar,’ said KPMG US Chief Economist Diane Swonk on X.”

The picture is mixed. The belief that March numbers represent a major setback is not supported by what appears to be a very mixed inflation picture.

Employment

“Employers added 303,000 jobs in March, the Bureau of Labor Statistics reported. The unemployment rate fell to 3.8% from 3.9% the month before.”

“Annual wage gains slowed to 4.1% from 4.3%, a trajectory likely welcomed by the Federal Reserve in its efforts to tame inflation but yet, a still-strong rate to help Americans recapture earnings that were decimated by the pandemic and high inflation.”

Consumer Behavior and Credit Standing

A corollary and subset to the issue of government deficits and government debt is found in consumer behavior. This Seeking Alpha piece reveals how personal money management is often debt-dependent, a behavior that threatens individual futures while posing a risk to the larger economy.

“Credit card delinquency rates reached their highest level on record in Q4 2023, according to a report from the Federal Reserve Bank of Philadelphia, while new mortgages appear to be riskier amid rising housing costs.”

“Nearly 3.5% of credit card balances were at least 30 days past due as of Q4-end. Stress among cardholders was further underscored in payment behavior, as the share of accounts making minimum payments rose 34 basis points to a series high from last quarter’s reading.”

While the past-due percentage is in check, it does suggest that many people carry significant credit card debt. This impression is borne out by the accounts of many people in sales that cannot complete transactions because the customer’s financial situation prevents purchase financing.

MarketWatch offered this take on U.S. consumer debt:

- U.S. household debt increased by 4.8% from November 2022 to November 2023, with credit card debt the single largest contributor to the increase at 16.6%.

- About a third of Americans said they expected to go into debt for holiday shopping in 2023.

- Roughly 25% of Americans were still holding on to 2022 holiday shopping debt ahead of the 2023 holiday shopping season.

“Household debt across all categories grew by 4.8% from Q3 2022 to Q3 2023, according to the latest

statistics from the Federal Reserve Bank of New York (FRBNY). This includes mortgages, home equity revolving debt, auto loans, credit cards, student loans and other consumer lending such as retail cards. The total household debt of $17.3 trillion entering 2024 is a new high for the U.S.”

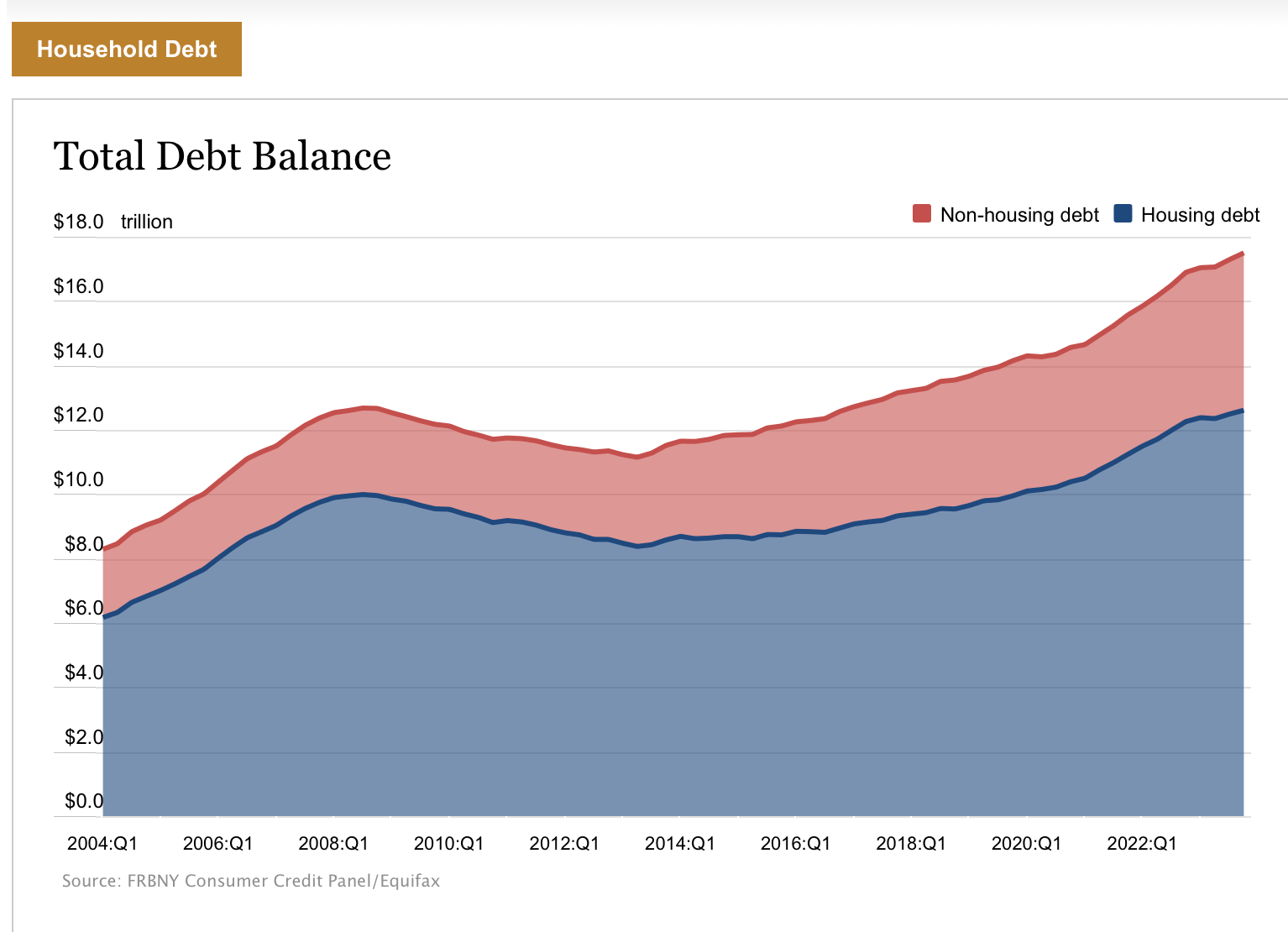

A view of the last 20 years of consumer debt patterns reveals a steady, persistent increase in both housing and non-housing categories:

{kind=link}

The largest increase in any category was credit card debt… home equity revolving credit saw the second-largest increase, growing by 8.4% over the same period. Auto loan and mortgage debt increased by 4%. Miscellaneous household, including retail cards and other consumer loans – also saw a substantial yearly increase of 7.7%.

The habit of large numbers of people “living on their credit cards” suggests that consumers may hit the wall at the same time. While this is a worrying development, it does not appear to have a direct impact on the markets in 2024.

Mortgage Struggles

The housing market continued to be challenging. Surges in prices combine with higher mortgage rates that are a byproduct of Federal Reserve interest rate raises in 2022-23 to discourage many first-time or less-than-wealthy buyers.

“Underscoring affordability issues, the median front-end debt-to-income ratio rose 500 bps from its Q4 2021 level, while median origination loan size and loan-to-value increased 9.3% and 900 bps, respectively, over the same period.”

Yet, demand for new housing remains strong overall. The demography of purchases based on income level may be skewed by mortgage rate increases, but demand is still strong overall.

- The median home-sale price as of February 2024 was $384,500, up 5.7 percent from one year ago, according to NAR data.

- The nation had a 2.9-month supply of housing inventory as of February, per NAR, which is low enough to be considered a seller’s market.

Monetary Policy: What Will the Fed Do?

A summary of the Fed’s actions at the March meeting featured the decision to hold interest rates firm at 5.25 to 5.50%, which the Fed has done since summer of 2023, when it last raised rates by .25%.

The Federal Reserve Board also stuck with its earlier forecast of three rate cuts before the year is out. This forecast is meaningful, as the Board of Governors monitors inflation constantly. It’s unlikely that it was surprised by the March inflation numbers.

Jeff Cox of CNBC explained both the decisions and forecasts. Cox pointed out that this rate (which banks charge each other for lending) is the highest in over 23 years of Fed policymaking.

Fed Chairman Jerome Powell commented at the March meeting:

“We believe that our policy rate is likely at its peak for this type of cycle, and that if the economy evolves broadly as expected, it will likely be appropriate to begin dialing back policy restraint at some point this year.”

Cox continues:

“The committee sees three more reductions in 2026 and then two more in the future until the fed funds rate settles in around 2.6%, near what policymakers estimate to be the “neutral rate” that is neither stimulative nor restrictive.”

Whether 2.6% is the correct level to achieve neutrality, the goal should be seen in the context of the Federal Reserve’s mandate of achieving maximum employment while keeping prices stable.

The minute meetings indicated that “almost all participants judged that it… appropriate to move policy to a less restrictive stance at some point this year if the economy evolved broadly as they expected,” the minutes said. “…they noted that the disinflation process was continuing along a path that was generally expected to be somewhat uneven.”

Federal Reserve Governor Lisa Cook, in a March 25 speech, offered a substantial explanation of the organization’s purpose and current policies:

“My main message is that, following a period of unusually high inflation and rapid monetary-policy tightening, inflation has fallen considerably while the labor market has remained strong. As a result of these welcome developments, the risks to achieving our employment and inflation goals are moving into better balance. Nonetheless, fully restoring price stability may take a cautious approach to easing monetary policy over time.״

Federal Reserve Quantitative Tightening To End?

The two primary tools that the Federal Reserve uses to set monetary policy are 1) interest rate levels and 2) quantitative easing or tightening. Dovishness generally translates to a combination of interest rate reductions and quantitative easing, by which the Federal Reserve adds securities to its balance sheet. This also provides additional liquidity to banks and helps push market interest rates lower.

Hawkishness is expressed in increasing interest rates and removing Fed-owned securities from the Federal Reserve balance sheet. The Federal Reserve has, in fact, been reducing its balance sheet by shaving about $1.5 trillion from Treasuries and mortgage-backed securities and by allowing up to $95 billion in proceeds from maturing bonds to roll off instead of reinvesting them.

The Federal Reserve did not suggest dates by which it intends to end these balance sheet reductions, but it did say at the March meeting that the roll-off pace would be cut by “roughly half” and the process should start “fairly soon.” Market economists expect the process to begin in the next month or two.

I believe that Jerome Powell and the Federal Reserve Governors are serious about working within its dual mandate of seeking maximum employment and price stability. The hawkish policy of 2022 and early 2023 is no longer required to push towards those goals; a neutral policy or gradual transition to a mild dovishness will probably achieve those ends.

Technology as a Secular Market Factor

Robyn Gibbard of Deloitte describes how technology is making for more efficient labor markets and a stronger economy:

“Artificial intelligence is today’s popular buzzword, but the increasing sophistication and availability of technology and software has already been replacing some jobs and creating new ones. This kind of transformation will continue – and since technological change is not always linear, there is always the possibility of fast changes that help boost productivity significantly. In this scenario, the average annual growth of labor productivity grows at an average annual rate of 1.9% per year from 2024 through 2028, compared to 1.6% in the baseline.”

I’m a believer in the power of technology (call it AI or just intelligent integrated computing or by another label) to increase the efficiency of many companies and to drive enhanced profits and revenues. This starts with companies producing the “picks and shovels” (Nvidia (NVDA), AMD (AMD), Broadcom (AVGO), Qualcomm (QCOM), etc.) and includes a set of powerful firms (Amazon (AMZN), Microsoft (MSFT), Google (GOOGL) and others) that build upon those technological tools to produce in-demand products for their corporate and individual consumers.

Technology is thus a large, growing and permanent component of both the economy and the stock markets. The deflationary benefits of categories such as artificial intelligence and high-speed computing create a secular trend that also drives deflation. This is a sea change and a fact of great promise for strategically-minded investors.

Potential Macro Surprises

Potential surprises – assuming these can be both for market better or market worse – exist. Some examples:

- Inflation defies the Fed’s modest optimism and trends up for the remaining three quarters of the year.

- Geopolitical tensions continue to rise, including the ongoing conflict between Ukraine and Russia, and rising tensions in the Middle East, including escalation between Israel and Iran. This could drive up energy prices to uncomfortable levels that hinder economic growth in the US and around the world.

- A US recession is triggered by a combination of corporate underperformance, a reduction in lending and borrowing.

- Real estate issues exacerbated by the 2022-23 Fed Reserve interest rate acts as a trigger for recession and/or a stock market decline.

- A true Black Swan emerges, perhaps a series of closely-bunched natural disaster or a massive pandemic.

I do not see a high likelihood for any of these outcomes. I believe inflation is, in fact, on a lumpy downward course. Geopolitics are a greater risk. However, if we look for example at the Russia-Ukraine conflict, the war has ground on for over two years and probably will continue in that mode. The risks and high human and infrastructure costs have not derailed the international economy, though they have certainly damaged specific nations and limited European economic potential.

I do not see signs of a significant oncoming U.S. recession, though recessions do exist elsewhere. Despite that, the markets are performing fairly well. The real estate situation in the US is complicated, but not in my opinion some equivalent of the 2007-8 mortgage derivative-originated financial meltdown.

Since Black Swans can’t be predicted, I view them as acts of nature better left alone in relation to predictions of market performance.

The November Elections

Given the ongoing dominance of the US economy and the influence of government policy on economics (federal, state and local), the November 2024 elections will indeed impact economies and markets. How much impact will depend on multiple factors, including the state of the economy in November (or January), potential shifts in economic policy (fiscal but also potentially monetary), and the influence of policy changes on corporate direction and strategies.

Should Donald Trump, the presumptive Republican candidate, defeat Joe Biden, the markets may react (in which direction is unknown). Since Mr. Trump has already had one term in office, a second Trump Presidency is something of a known economic-market quantity.

If President Biden returns to office, I see a relatively small effect, given the familiarity of observers and investors with Biden’s economic policies.

Partisan opinion will flourish no matter the election outcome, but starkly different political leanings of voters do not impact mass economic or investing behavior in a fundamental way. That is what history says, in any case.

Summary

The well-known market bull, Tom Lee of Fundstrat, sees the S&P rising over 10% from current levels to reach, 5700 by year’s end.

Lee appeared to be optimistic on Friday, calling this week’s retreat in stocks a “temporary moment of pain and a buy-the-dip opportunity.”

“I think the narrative got muddled because that CPI report was a disappointment, but it was driven by what we call stubborn components: shelter, auto insurance … the median core CPI component now has only 1.7% Y/Y inflation. I mean, inflation is normalizing, it’s just not evident in the total picture,” Lee told CNBC.

Tom Lee compares the collective PE to the US 10-year Treasury as a basis for calculating what the median PE should be. And when the 10-year is around the current level, that number is 20.

He also responds to the near-consensus on an overvalued market, saying “… if you look at the median stock, it is actually at 16 times.” This is essentially a way of subtracting some of the distorting effects of The Magnificent Seven.

While I’m not enthusiastic about factoring out the technology companies, since I see them as increasingly driving the economy, I believe that historical PE ratios are also not laws of physics. So, if technology is making economies more efficient, then many smart companies will prosper and support higher ratios.

I also believe that the fears about 1) inflation returning to dangerous levels and 2) Federal Reserve policy reverting to hawkishness are exaggerated. I believe that the Federal Reserve is committed to its dual mandate, and will keep on with a neutral or slightly dovish set of policies. I think there will be at least two interest rate cuts and that quantitative tightening will wrap up soon.

For the remainder of this year, I hold a moderately bullish view of both the economy and the markets.