Patria Investments: Go Local In LatAm

Adam Gault/OJO Images via Getty Images

Investment Thesis

Patria (NASDAQ:PAX) is a global alternative asset manager and industry leader in Latin America, with over 35 years of history, combined assets under management of $31.8 billion, and a global presence with offices in 10 cities across 4 continents. Patria aims to be the gateway for alternative investments in Latin America. Through a diversified platform spanning Private Equity, Infrastructure, Credit, Public Equities and Real Estate.

Patria is a well established leader in the Latin American alternative investment arena. The company has a strong reputation in the global alternative asset management community, which is evidenced by the large number of assets under its management that are sourced from international institutional investors.

The company has steadily grown assets under management despite a challenging macroeconomic landscape in the region. Compared to global peers, the current price offers a compelling valuation for long term capital appreciation, while in the short term, the company pays a healthy 8% dividend with no withholding tax retained.

LatAm offers long-term growth via its growing population and maturing economies. The region is set to return to economic growth mode, making this a good time to add exposure.

The Company

Patria was founded back in 1988, in partnership with Salomon Brothers, a leading global investment bank. A key contributor to its development was a subsequent investment and partnership with Blackstone (BX). This lasted for over a decade, until 2022, during which time Patria management absorbed significant expertise and best practice in alternative asset management. In 2021, Patria IPO’d with a listing on the Nasdaq, creating a capital event which triggered an exit by BX from its direct investment in Patria.

Patria is incorporated in Grand Cayman. This often seems to concern investors, but it is actually, in my mind, a positive. Cayman is a well established offshore financial centre which has strong governance and access to management talent. It is a highly tax efficient jurisdiction for a business which sources assets globally and invests in multiple countries. There is no withholding tax on dividends for investors.

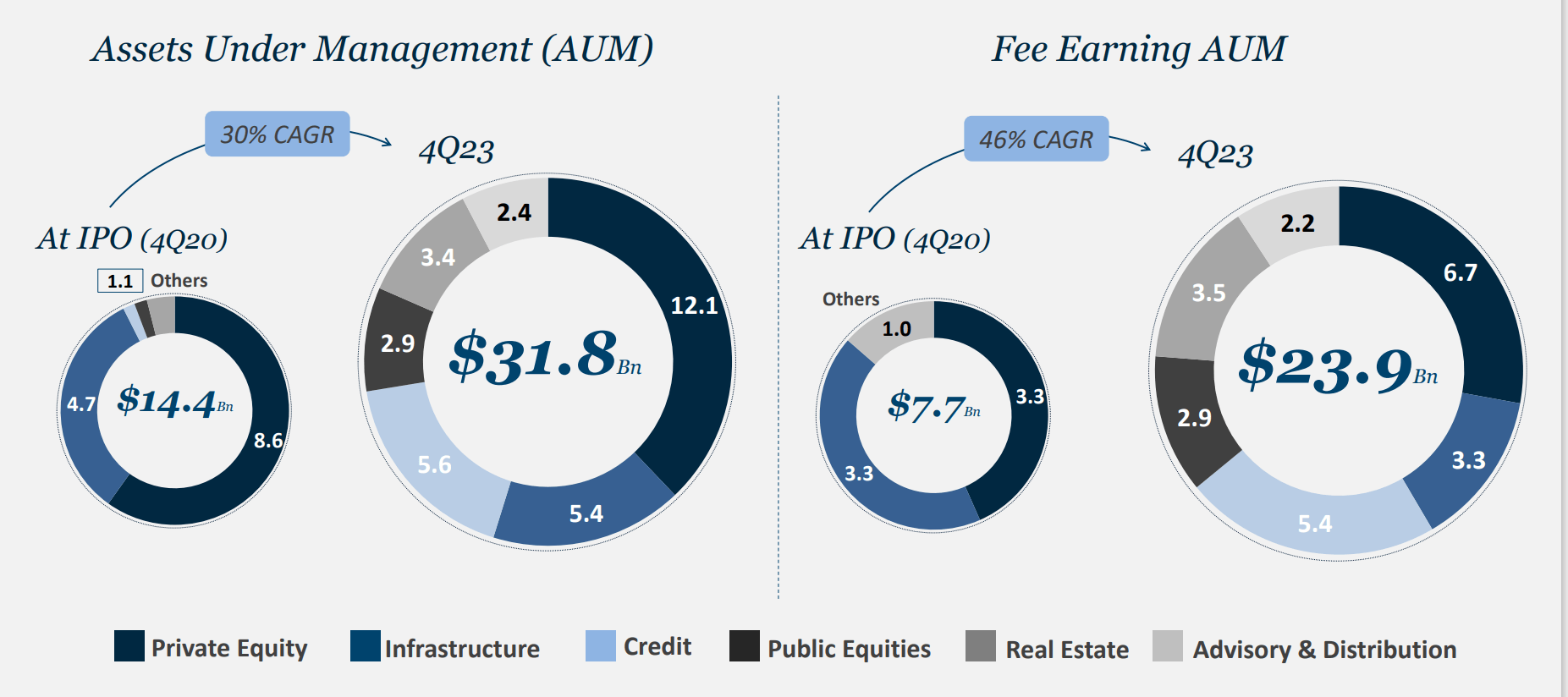

Assets Under Management

In the short period since the IPO, the growth of the business has been stellar, with a growth in Assets Under Management from $14.4bn to $31.8bn, to year-end 2023, a 30% CAGR. Importantly, of the AUM, a large proportion of the new AUM mandates are fee earning, with fee earning AUM growing by a CAGR of 46%.

{kind=link}

The distinction here is that a proportion of alternative asset mandates are committed by investors, but not yet invested by Patria, representing ‘dry powder’ or assets targeted at unclosed transactions. Only once deployed, do Patria generate management fees. Another way to look at the non fee earning assets is as a future earnings pipeline, with high execution confidence.

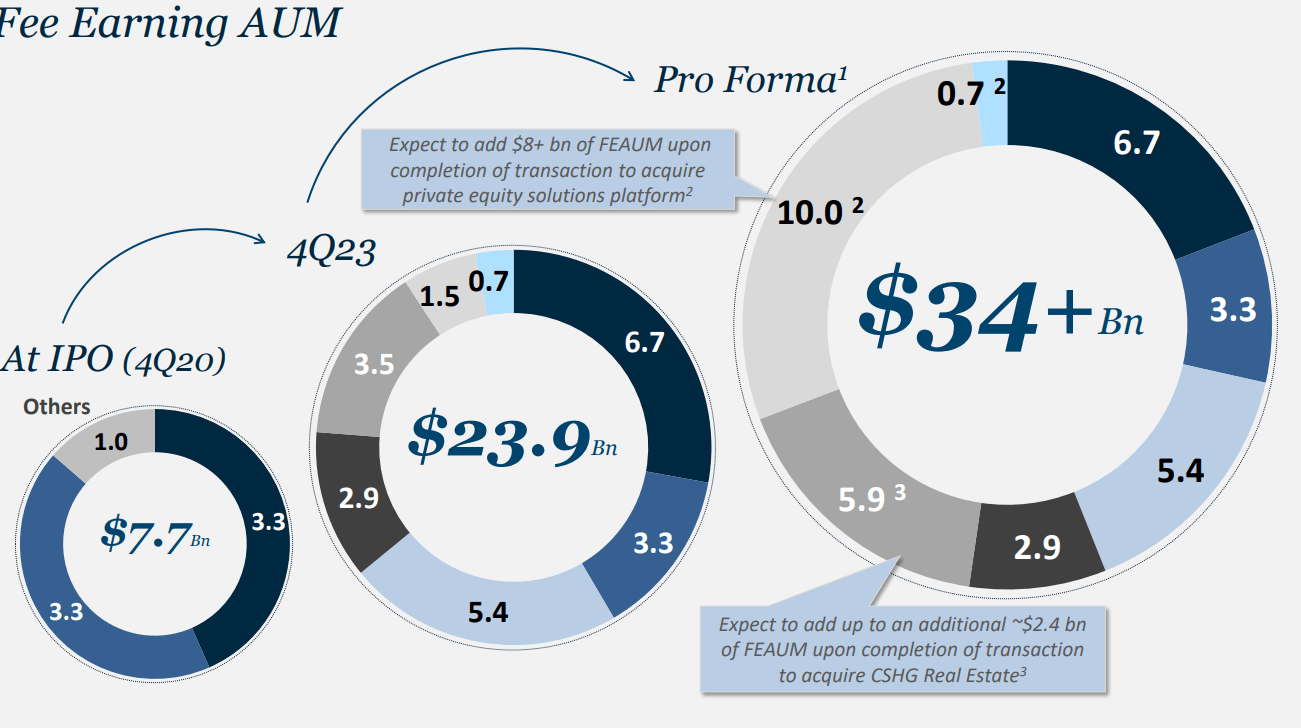

Looked at this way, the earnings currently reported are based on the fees from $23.9bn of assets, which means the remaining $8bn of AUM is not currently contributing to earnings, but will do so once deployed in new investments.

In late 2023, Patria agreed to acquire a new Private Equity platform, and Credit Suisse’s LatAm Real Estate franchise. Both transactions are expected to close in H1 2024, increasing the fee earning AUM to $34bn on a pro forma basis.

{kind=link}

Business Segments

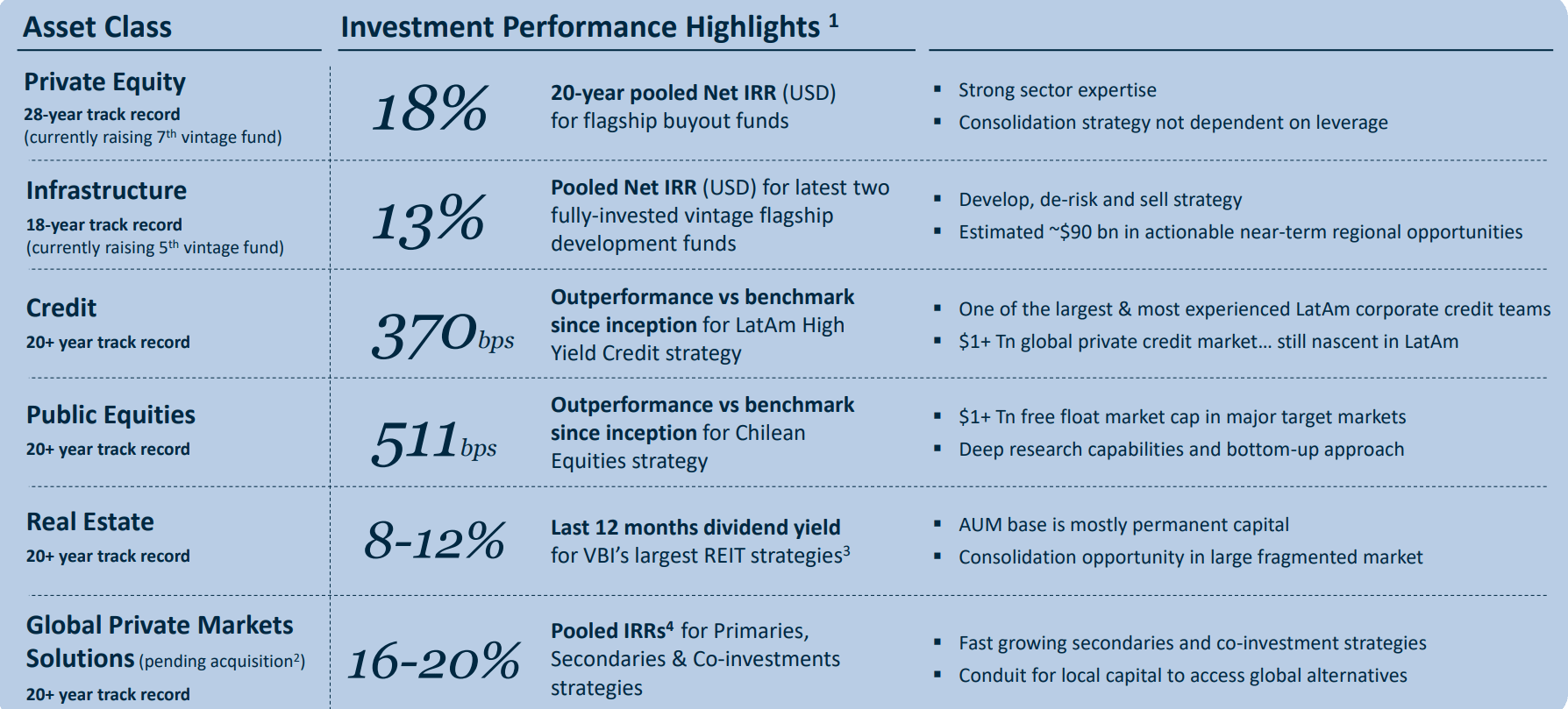

Patria operates in four key business segments: Private Equity, Infrastructure, Real Estate, and Credit.

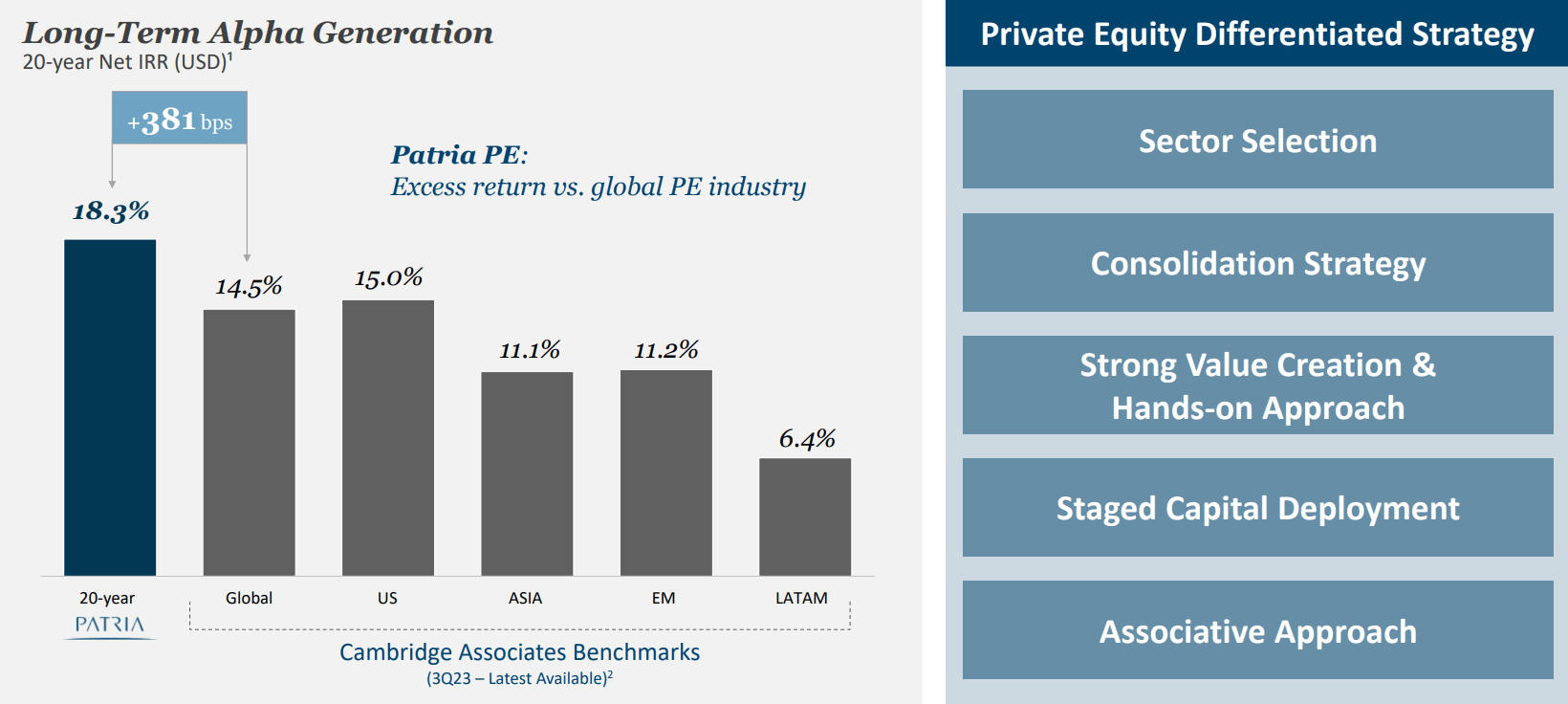

All segments have an impressive track record of IRR and benchmark outperformance, over long periods. This through cycle track record which supports the growth in AUM.

{kind=link}

Private Equity

This unit creates partnerships with entrepreneurs throughout LatAm to deploy client’s capital in support of business ventures engaged in transforming key areas of the regional economy. Focus areas are, Agriculture, Healthcare, Logistics, Shopping Malls, and Gated Communities. Private equity is the largest portion of AUM, with over a third of the total. The track record of outperformance in all regions is striking.

{kind=link}

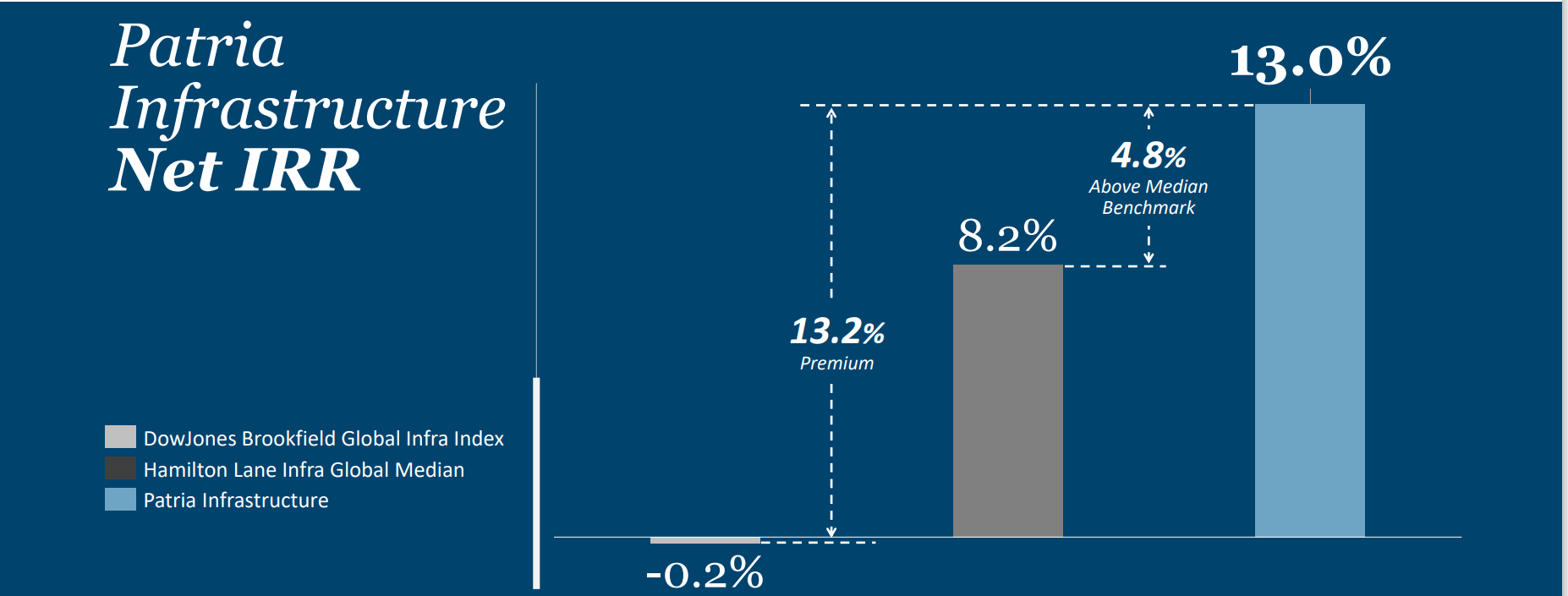

Infrastructure

As a developing region, infrastructure investment is a key growth theme. Patria deploys client’s assets to invest in the key focus areas of Data Infrastructure, Environmental Services, Logistics, Power and Energy, and Transportation. Roughly 17% of AUM is at work in the Infrastructure space. IRR has beaten the global benchmark by over 50%. Management sees $90bn of actionable investment opportunities by the end of the decade.

{kind=link}

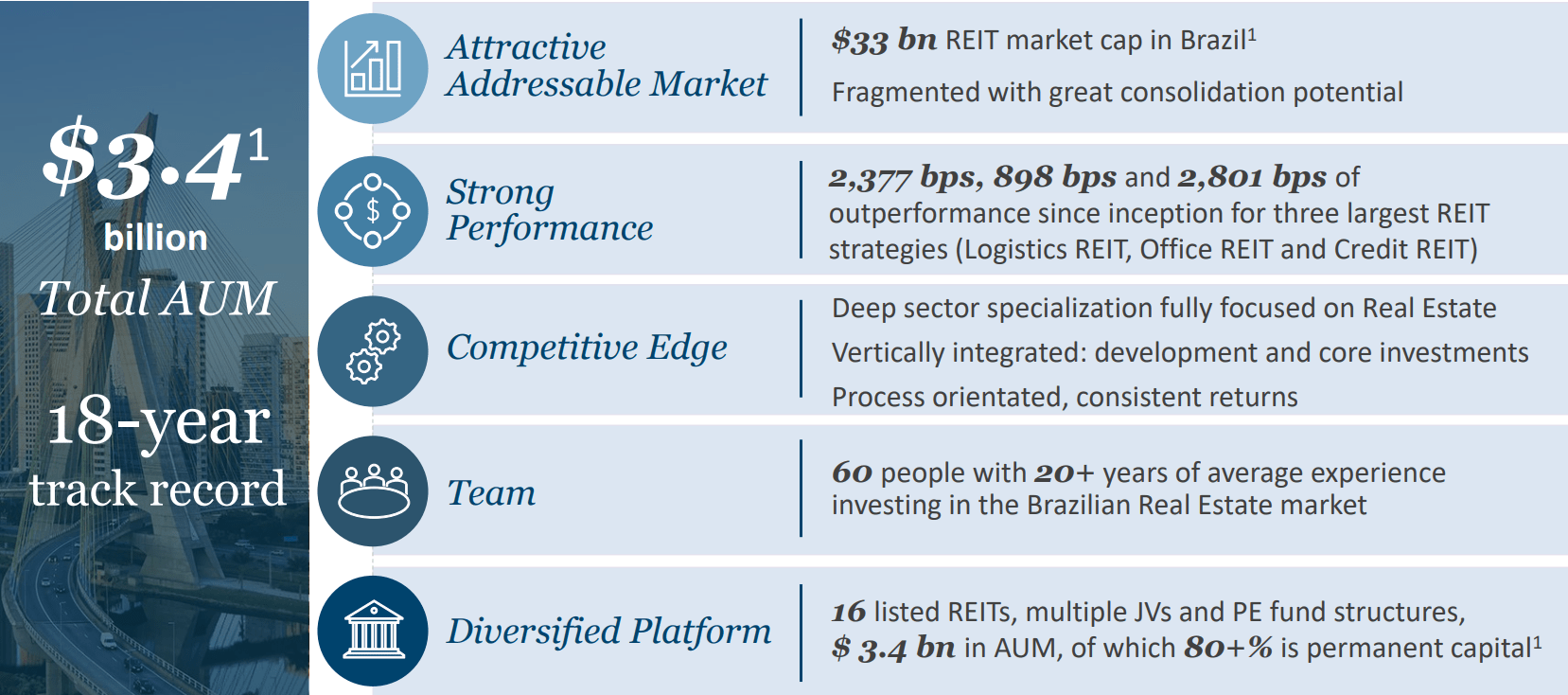

Real Estate

Patria invests in real estate, and agricultural land. This segment represents about 10% of the total Assets Under Management. Activity is both via REITs and Individual projects. Given the current challenges in the Commercial Real Estate market, this segment needs some attention. The business is based in Brazil. Key segments are Logistics, Office, and Credit.

Here again, Patria has an impressive performance track record – outperforming the benchmarks by between 0.9 and 2.8% IRR. It’s important to note that 80% of the AUM is in the form of permanent capital. This means that interest rate risk, the key challenge facing the sector, is limited. Furthermore, important is that this is an asset management business, with clients’ money mainly at risk.

{kind=link}

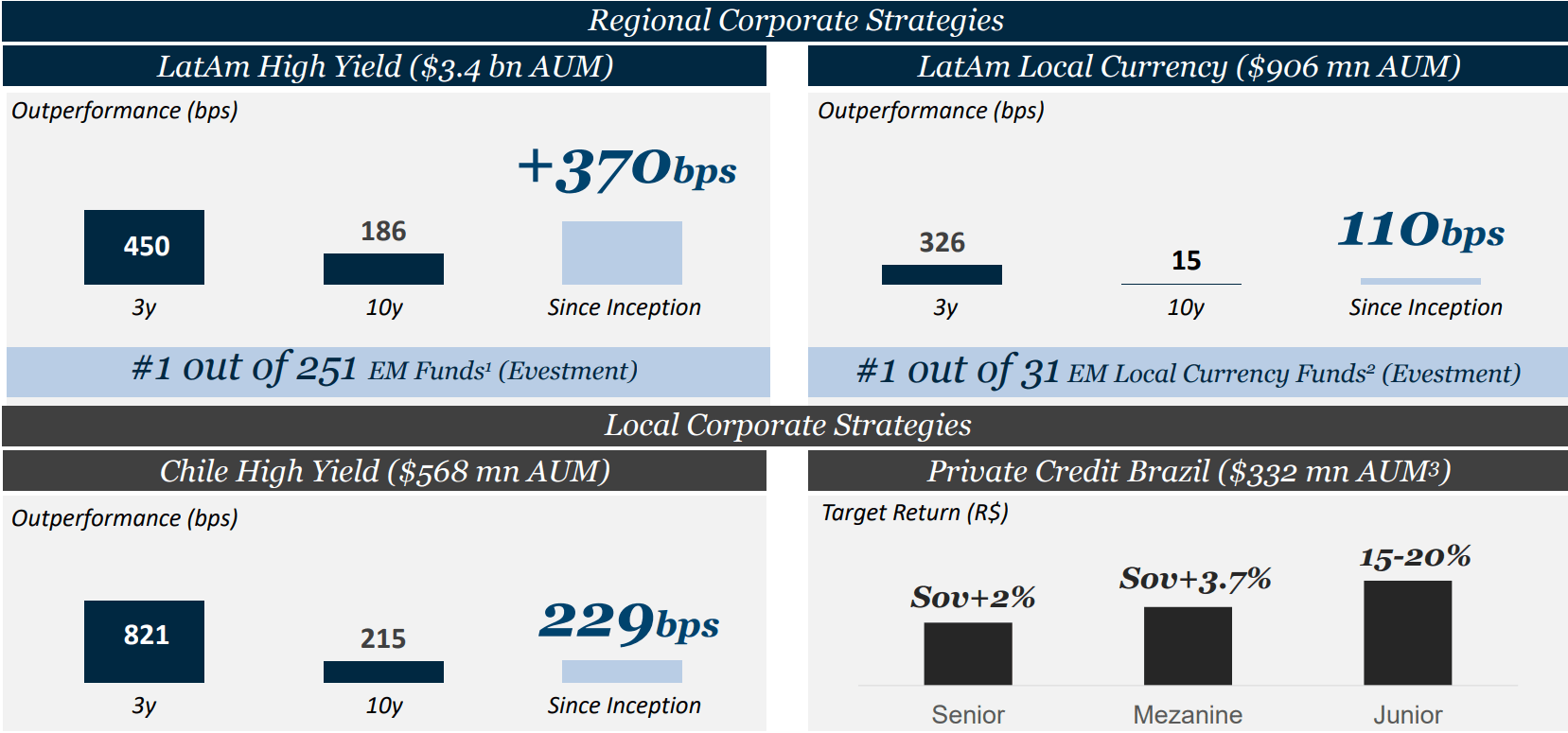

Credit

Patria is an active player in providing corporate credit to LatAm companies. The credit business is about 17.5% of AUM. A few years ago, the author had the opportunity to visit the head office of the credit business, and I was impressed by the underwriting standards, portfolio management, and risk management approach. One of the reasons that Patria has been on my radar stems from this positive experience. Seeing strong benchmark outperformance is no surprise to me.

{kind=link}

The balance of AUM is in the smaller Public Equity and Advisory & Distribution segments.

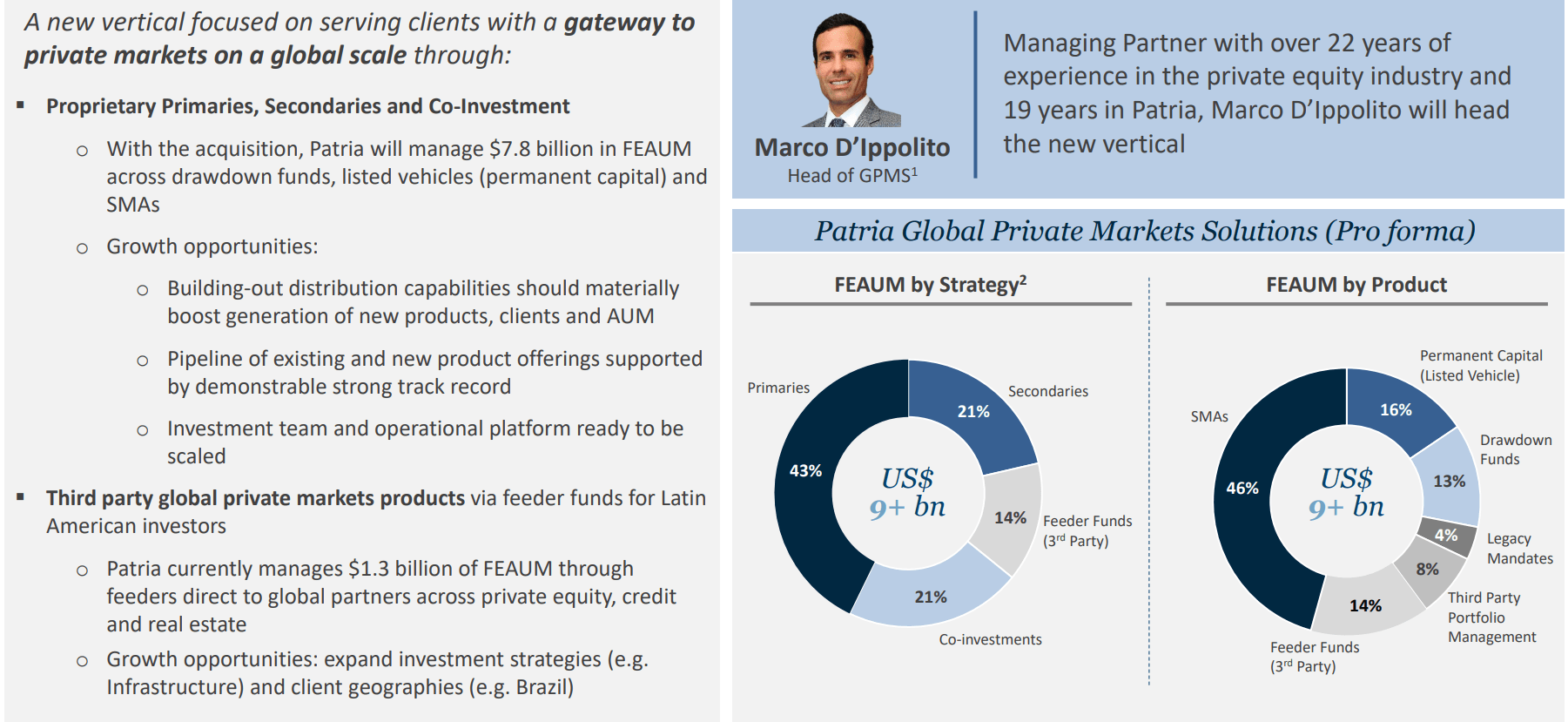

The New Acquisition

As discussed above, a major acquisition of Private Equity Solutions is due to close in H1 2024. Patria are building this into a new vertical business practice, Global Private Markets Solutions. This will be led by Marco D’Ippolito, a longstanding Patria executive, who will ensure that the existing significant business is expanded by integration into the Patria LatAm network.

{kind=link}

Business Performance & Outlook

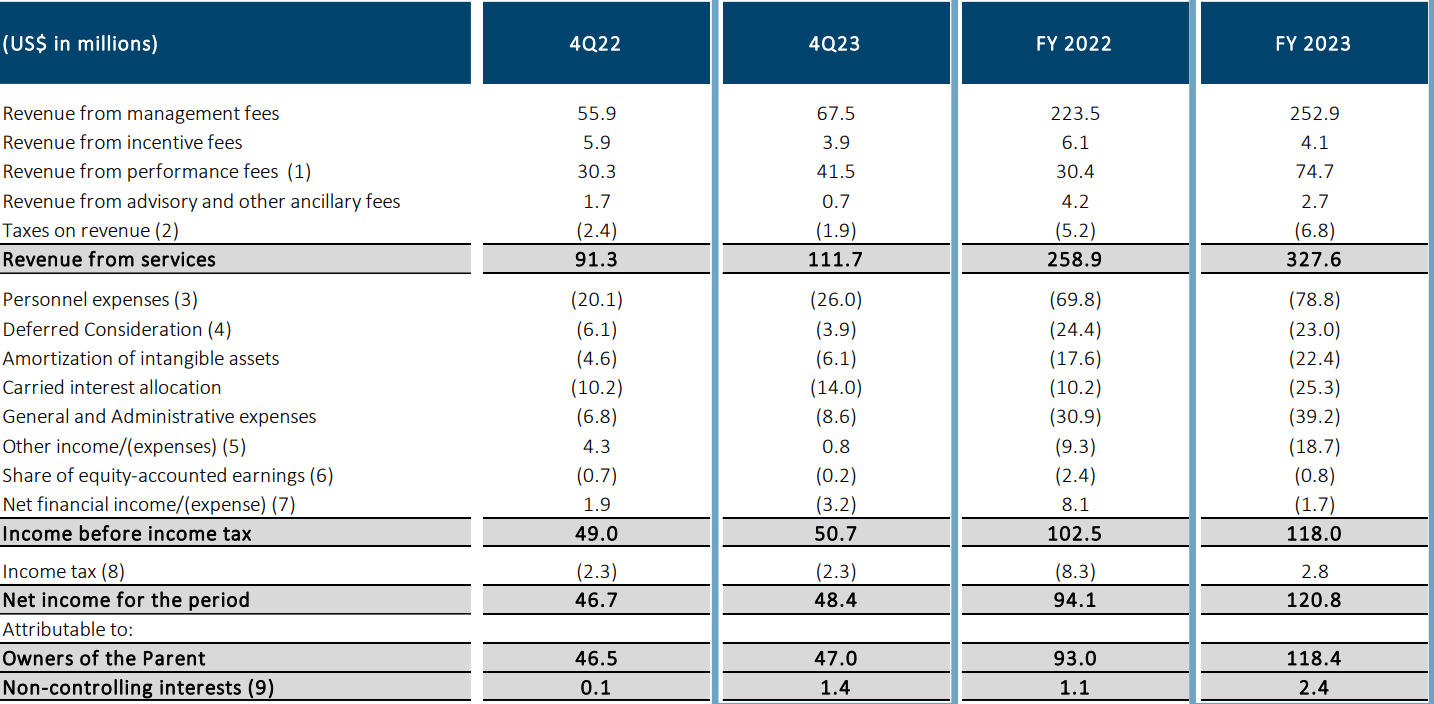

Patria released FY 2023 earnings 15th February. Given the growth in AUM and fees, it’s not surprising to see great numbers. Key highlights on the full year performance from the analyst presentation and earnings call:

- Revenues up 26.5% YOY to $328m

- Net income up 128%

- AUM up 17

- Fee related earnings to grow by 15% to 2025.

- 2025 goal of $20bn capital generation to be realised in 2024 (a year early, which is impressive with the goal set only in 2022)

- 70% of fee earning AUM in hard currency (USD, EUR, GBP)

- Fees for transactions closed in 2023 only $2m of 2023 earnings – full realisation in 2024.

- Acquisition funding. Funding often by seller’s financing, with consideration deferred, and sometimes by a share of Patria’s ongoing revenues. Not funded by debt, or cash up front.

{kind=link}

LatAm Economic Outlook

The regional economies growth story is founded on the demographic profile. The median age is only 32 years, with a young population still to reach economic maturity. While population growth has slowed to 0.8% per annum, forecasts are for peak population to only hit in 2056. This implies decades of workers productivity and economic growth ahead.

Population Pyramid

The flip side to this is that the region has many structural inefficiencies and sociopolitical challenges, the ‘growing pains’ of the young.

The World Bank recently updated its economic outlook for LatAm. Short-term growth is expected to be muted, at 1.6% for 2024, improving to 2.7% in 2025, and 2026.

This implies growth, but continued short-term challenges. LatAm investment is a long game.

I see positives for Patria here as a homegrown asset manager. The institutions that place assets with them are looking for long-term growth and global diversification. They need exposure to the continent, but given the risks, will want to be cautious. Here the Patria track record becomes an asset magnet.

Valuation

On a forward PE basis, Patria is cheap compared to peers. The PE discount to Apollo – the next closest, is over 50%. Blackstone and Ares are around twice the price of Apollo.

Why the discount?

- Peers are well established… Patria has been around for 35 years.

- LatAm is risky… Patria has a track record of outperforming global peers on IRR.

- Cayman is not a credible jurisdiction… not so. Cayman has long been a leading location for financial services, and has strong governance, plus superb tax efficiencies.

- CRE exposures… less than 10% of AUM, permanent capital (no interest rate risk.)

- LatAm currencies aren’t stable… 70% of income is in hard currency.

Analysts are generally positive. SA analysts and Wall St. both have Buy ratings, while SA Quant has a Hold.

Seeking Alpha

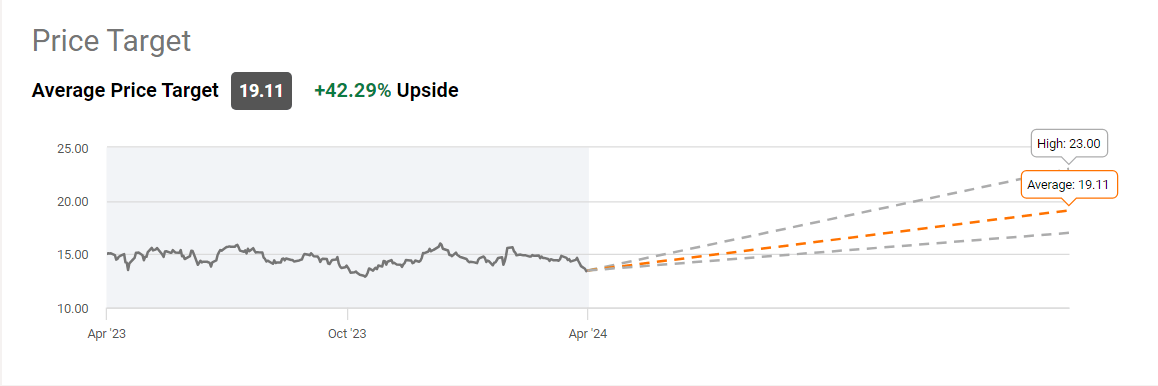

Wall Street has an average price target of $19.11, a 42% upside to current pricing.

{kind=link}

Digging into the SA Quant rating, the issue there is the market momentum.

Seeking Alpha

The stock just can’t get a bid, despite great growth and profitability, and a B+ for valuation. I am not sure what peer valuation is considered here.

Risks

I think that as an alternative asset manager solely focused on an emerging market region, there are risks aplenty. However, I think that most of those specific to Patria are controlled. Key concerns:

- Growth in AUM constrained.

- Brazil specific political event.

- Credit crisis.

- Integration risk of the new PE platform.

- A hyperinflation country event.

- Human talent risk.

My Take And Position

I think that this is an exceptional business, which is well managed, well connected to business locally and to capital markets globally.

It has a proven track record of outperformance on a global level. This attracts assets.

The market is mispricing this business, which can be expected to produce at least 15% growth in profit annually while paying out an 8% dividend, but is priced at a forward PE multiple of less than 10.

I have a current long position, and will add to this at the current pricing levels, plus selling puts to average down if the price continues to fall. This is a long-term position for me.