Rocket Companies Is Materially Overpriced Considering The Interest Rate Outlook

ZargonDesign/E+ via Getty Images

What Rocket is – a mortgage banker, not a fintech

Rocket describes itself as follows in its 2023 10-K:

“We are a Detroit-based fintech company including mortgage, real estate, and personal finance business. We are committed to delivering industry-best client experiences through our AI-fueled homeownership strategy. Our full suite of products empowers our clients across financial wellness, personal loans, home search, mortgage finance, title, and closing.”

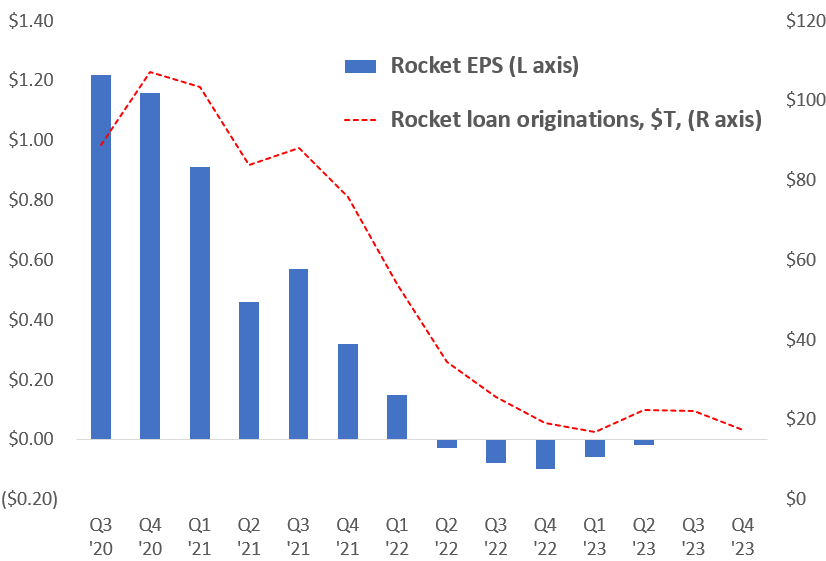

Note the politically correct buzzwords – “fintech”, “industry-best”, “AI”, “full suite”. But in fact, Rocket’s earnings are tied closely to its loan origination volume, as this picture shows:

{kind=link}

Sources: Rocket financial reports

Statistics (regression analysis) say that 83% of the change in Rocket’s EPS since it went public is due to changes in its home mortgage loan originations. The small remainder in EPS changes was probably due to the natural hedge of loan servicing income and expense management. No evidence of “fintech” or “full suite”.

And while Rocket pitches that it is “industry-best”, 96% of the changes in its loan originations since it went public were due to changes in national home mortgage origination volume (again as measured by regression analysis), not its own behavior. So it is fair to say that Rocket’s EPS outlook over the next few years will be very largely due to the direction of U.S. home mortgage originations.

What is the outlook for U.S. mortgage originations? Better, but still weak

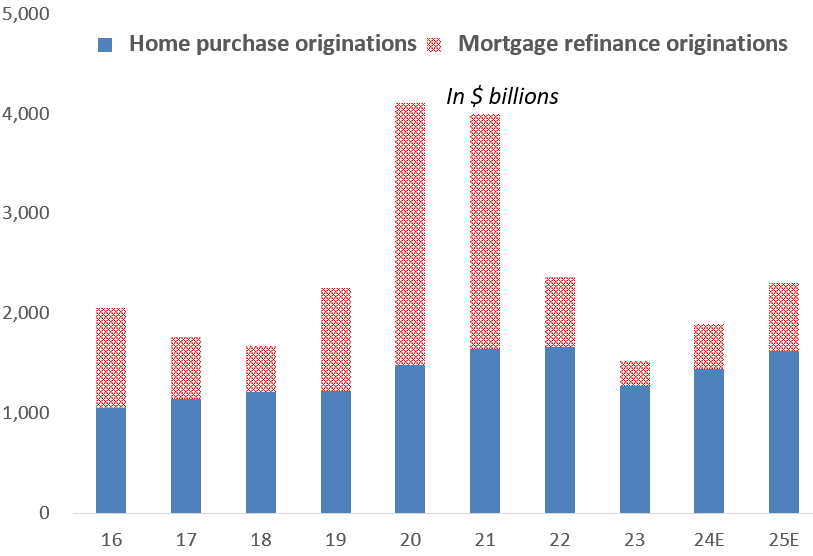

Let’s start with Fannie Mae’s outlook:

{kind=link}

Source: Fannie Mae

This chart makes several important points:

- Fannie Mae expects mortgage originations to rise this year and next year, but to be way below the levels achieved in 2020 and 2021.

- Mortgage originations related to home purchases are relatively stable. They surged during the low-mortgage rate/home nesting COVID years, but Fannie Mae expects a rough return to normalcy by next year. Fannie Mae’s ’25 forecast represents a 5% annualized growth rate from ’16.

- The volatility in mortgage originations over time is clearly due to refinancing activity. Refinancing activity rose by 460% from ’18 to ’20 and then fell by 90% by ’23.

If Rocket’s EPS is going to rise sharply, then, home mortgage refinancing activity is going to have to materially increase. Fannie Mae does see a pickup, from $250 billion in ’23 to $685 billion in ’25. That still leaves Rocket’s earnings well short of what is needed to support the current stock price (see below), but I believe even Fannie Mae’s forecast is optimistic, for two reasons:

1. A large percentage of outstanding mortgages have very low rates. Today’s 30-year fixed rate mortgage rate is 6.9%. But according to a Redfin report, as of September of last year, 79% of the outstanding mortgages in the country today had 5% or lower interest rates, and 59% were below 4%. Only 11% had 6% or greater rates. So a substantial rise in refinancing originations will require a substantial decline in the mortgage rate, at least down to 5%.

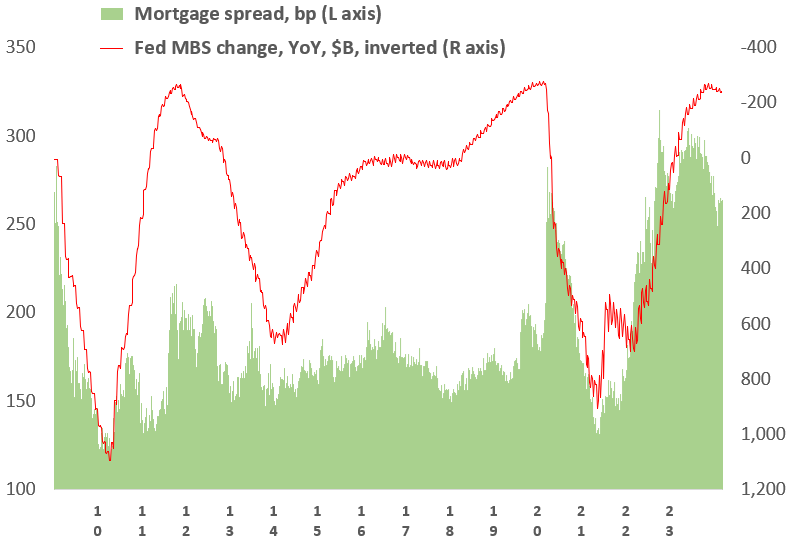

2. The Federal Reserve is not promoting lower mortgage rates. The Fed can do so in one of two ways. One is to buy mortgage-backed securities (MBS). The Federal Reserve is a huge player in the mortgage investment market. It currently owns about 20% of all outstanding U.S. mortgage debt. This chart shows that the Fed’s buying and selling has had a major impact on the mortgage yield compared to a 10-year Treasury bond yield:

{kind=link}

Sources: FRED

But the chart shows that the Fed is now reducing its MBS holdings. The chances are slim that in the foreseeable future, the Fed will start buying MBS again to help lower mortgage rates. In fact, we heard this recently from a Fed Governor:

“The Federal Reserve should shed the roughly $2.4 trillion in mortgage-backed securities on its balance sheet, said Federal Reserve Governor Chris Waller. ‘I would like to see the Fed’s agency MBS holdings go to zero,’ Waller said.” (MarketWatch, March 1, 2024)

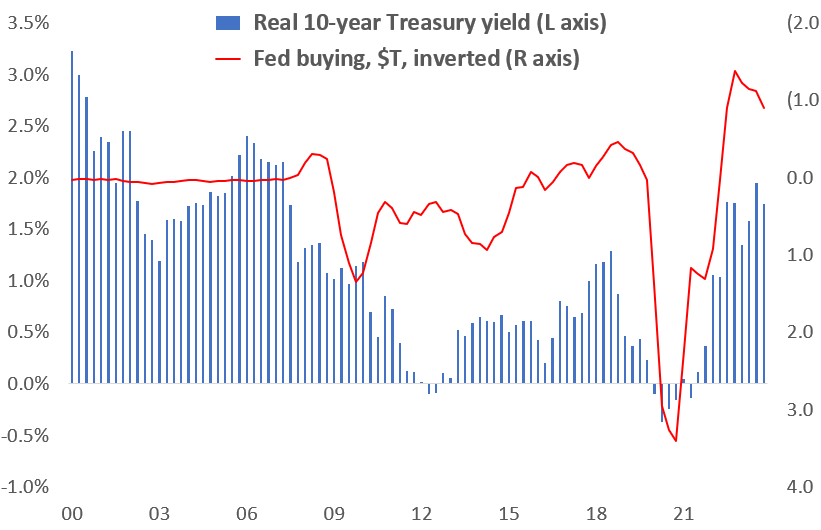

Another way for the Federal Reserve to lower mortgage rates is to lower real 10-year Treasury rates. Again, the Fed’s tool to do so is to buy long-term Treasury bonds. But again, the Fed is reducing its Treasury holdings, as this chart shows:

{kind=link}

Sources: FRED

It is clear that the short end of the yield curve will decline as the Fed lowers its funds rate over the next couple of years. But it is not clear that the long end of the yield curve, the end that counts for mortgage rates, will fall much, if not all. It is more likely that the yield curve will return to more normal steepness. That would leave the mortgage rate over 6%.

Here is what Fannie Mae’s mortgage origination forecast means for Rocket’s EPS outlook

Without Fed support, then, even a moderate refinancing boom seems unlikely. So I view Fannie Mae’s mortgage origination forecast as optimistic. Putting Fannie’s forecast into my EPS regression model results in EPS of ($0.12) this year and $0.25 next year. Seeking Alpha’s summary of Wall Street analysts’ forecasts for Rocket are $0.32 for this year and $0.57 for next year. As I said above, my model doesn’t fully capture the stabilizing impact to Rocket of its loan servicing earnings and Rocket’s probably ongoing cost-cutting efforts. I will therefore sign on to the analysts’ estimates.

What is Rocket worth?

Financial stocks can be valued by both a P/E ratio and book value per share. Let’s start with the book value.

Book value valuation. Rocket’s book value includes assets less liabilities plus the present value of its loan servicing business. They total $4.60 per share in value. Rocket’s current stock price is $14.55, so investors have assigned a $10 per share value to Rocket’s loan origination business plus its “fintech” businesses.

What might Rocket’s fintech business be worth? According to page 63 of its 10-K, revenues of Rocket Money, Rocket Homes, and Rocket Loans totaled $267 million last year. That is only $0.13 a share. Actual earnings weren’t given, but were almost certainly a loss. I’d give these businesses nearly no value. But investors see magic in fintech, so let’s give them a $1 billion valuation. That’s $0.50 a share.

That implies a $9.50 per share for Rocket’s loan origination business, or $19 billion. Peer UWM originates more than Rocket, and its origination business is valued at $9 billion. The $10 billion difference is $5 a share. So a book valuation makes Rocket’s $14.55 stock price suspect.

P/E valuation. What is the “right” P/E valuation for Rocket? We know that the faster the growth rate, the higher the P/E. A company’s growth rate can be then broken into its industry’s growth rate and its market share changes. Here’s how those factors shake out for Rocket:

Industry growth rate – low single digits. Because mortgage lending volume is so volatile, it is important to measure growth rates from similar environments. I used the starting year of 1994 when higher interest rates killed off a refinancing boom, similar to today. The annualized growth rate of home mortgage volume since then? A measly 2%. Future growth is unlikely to be much better because homeowners are currently holding such low-rate mortgages.

Rocket’s market share – growing, but not always. From its start-up in the 1990s, Rocket reached a 9% share in 2020. But its most recent share was 5%. The problem is that Rocket’s direct-to-the-consumer business model is strong for refinancing, but not for home purchases, where relationships with realtors are important. I estimate that Rocket has a 10% refi share and a 3% home purchase share. I expect Rocket to gain share going forward, but strong share growth is far from guaranteed.

Net/net, I will estimate 5-7% annual origination growth for Rocket. In my view that doesn’t warrant more than a 12 P/E, about average for a financial company. Applying that to Rocket’s expected ’25 EPS of $0.57 gives a $7 target price. By my calculations, that’s less than the current $15 price. If you got it, sell it.

Where I could be wrong

Rocket truly becomes a fintech. As I noted above, its non-mortgage banking businesses are a rounding error today. And its current fintech efforts – consumer financial services, real estate brokerage, and consumer lending – are all in mature and highly competitive businesses. But I guess you never know.

Takeover? Does some large bank or other entity decide it wants to make a big splash in mortgage banking? Banks have been edging away from this year for many years, so unlikely. But…

Reduced competition. Competition has declined since the recent refi boom faded. Some peers shut down, all slimmed down. There are certainly more reductions to go. Enough to materially increase Rocket’s profit margin and allow it to resume share growth? We’ll see.

Disinflation/deflation could push mortgage rates below 5%.

A serious recession could get the Fed back in the business of supporting the Treasury and MBS markets.