The S&P 500 Breaks Through 5,000

Yuichiro Chino/Moment via Getty Images

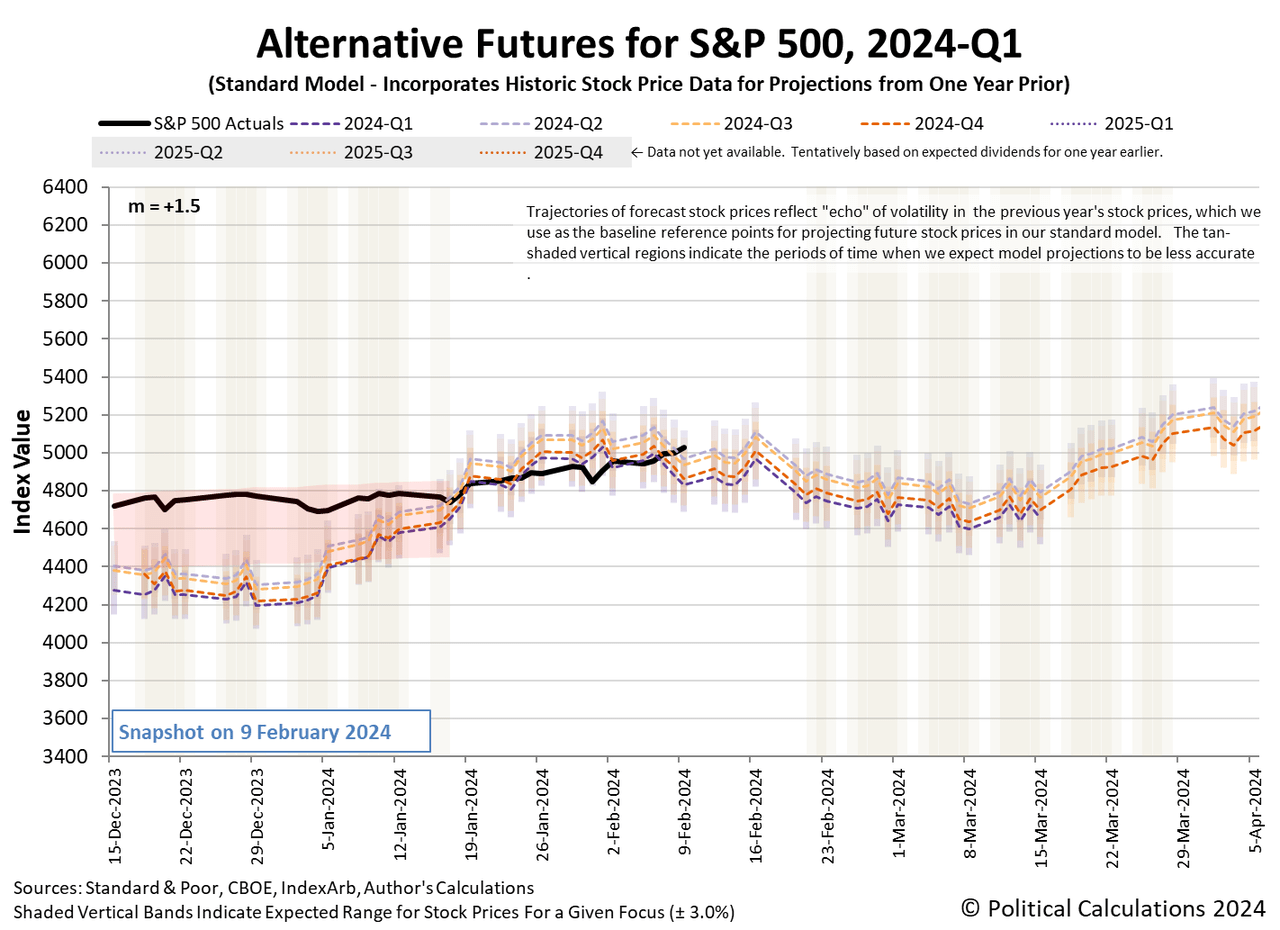

The S&P 500 (Index:SPX) rose a little under 1.4% over its previous week’s close, breaking through the 5,000 level on Friday, 9 February 2024 and wrapping up the week at a new high of 5,026.61.

Much of that boost came on the strength of a rally in megacaps, which is to say the stocks of the companies with the largest market capitalizations in the U.S. stock market.

The move also coincides with a transition in how far into the future investors are focusing their attention. Investors have shifted their forward time horizon from 2024-Q1 to 2024-Q2. That matches the strengthening expectation the Federal Reserve will hold off on starting a series of rate cuts during the second quarter of 2024. As for why that expectation strengthened, it had a lot to do with Federal Reserve officials sending the message they are going to hold off cutting rates until later in 2024.

Here’s the latest update for the alternative futures chart, where we find the trajectory of the S&P 500 is consistent with investors focusing on 2024-Q2 in setting the level of the index.

{kind=link}

{kind=link}

The week came with a big political story in the United States, which broke on Thursday, 8 February 2024. The story is the U.S. Department of Justice’s announcement it would not file criminal charges against President Joe Biden for the willful mishandling of classified documents going back to his time as Vice-President during the Obama administration. The special prosecutor investigating the matter declined to file charges in part because of the President’s age and failing memory would make it difficult to obtain a conviction in a jury trial.

That announcement was followed with President Biden’s evening press conference, which has been described as “an all-time PR blunder” because it raised further questions of his mental acuity and fitness to continue in office.

We’re discussing the story to make a point that matters to investors. This is a political story that has a direct bearing on the future of the U.S. government. With the 2024 presidential election campaign well underway and setting up to be a rematch between Joe Biden and Donald Trump, it’s a story that can very much affect what investors expect for the future. If Biden steps aside, whether in running for reelection or in even finishing his current term as President, the outcome of that action will create new uncertainties for investors. Increased uncertainty has a negative effect on stock prices.

All this news broke well ahead of when markets opened on Friday, 9 February 2024, so investors had ample time to absorb its impact. The S&P 500 would rise 0.6% to break through the index’ 5,000 milestone and close at an all-time record high that day. For something many might think would have a negative effect, that effect would appear to be minimal.

That’s not because investors had somehow mysteriously already priced that new information into the market beforehand. Nor is it because investors are ecstatic at the prospect of a future without Biden as President. Nor is it because investors are rejecting what the DOJ’s report and the press conference revealed about President Biden. Historically speaking, unless changes in tax rates are involved, what politics contributes to stock prices is virtually indistiguishable from noise. Noise that gets easily lost among the more serious factors that drive stock prices.

Which is why we almost never feature political headlines when recapping the market-moving news headlines of the week that was, although we’re making an exception this week and are presenting three political headlines just to drive that point home. Here are the week’s headlines:

Monday, 5 February 2024

- Signs and portents for the U.S. economy:

- Fed officials claim they’re being prudent in setting timing for rate cuts in 2024:

- Bigger trouble developing in China:

- Bigger stimulus developing in China:

- Some positive recovery signs in Eurozone:

- Nasdaq, S&P 500, Dow slump and yields rise with Fed ‘likely overstaying their welcome’

Tuesday, 6 February 2024

- Signs and portents for the U.S. economy:

- Fed officials setting the table for rate cuts later in 2024:

- Bigger bailout developing in China:

- BOJ officials thinking about ending never-ending stimulus in 2024:

- ECB officials follow Fed officials in pushing back on rate cut expectations:

- “Some” signs of economic rebound in Eurozone:

- Nasdaq, S&P, Dow eke out gains as Fed speakers largely reiterate caution on rate cuts

Wednesday, 7 February 2024

- Signs and portents for the U.S. economy:

- Bigger trouble developing in China:

- JapanGov official claims BOJ officials plan to end never-ending stimulus won’t mean stop in fight to end deflation:

- S&P 500 closes just below historic 5,000 mark as tech stocks rally; Nasdaq, Dow also rise

Thursday, 8 February 2024

- Signs and portents for the U.S. economy:

- Fed officials are optimistic but not confident:

- Bigger trouble developing in China:

- BOJ officials say end of never-ending stimulus to be slow, will stop taking so many risks:

- Bigger trouble developing in Eurozone:

- ECB officials to stand by before doing anything about bigger developing trouble:

- S&P 500 ends just shy of 5,000 mark after touching milestone

Friday, 9 February 2024

- Signs and portents for the U.S. economy:

- Fed officials say no need to hurry on interest rate cuts:

- Bigger trouble, stimulus developing in China:

- ECB officials get data indicating easing inflation in Eurozone:

- S&P consolidates above 5,000 points for first time ever, Nasdaq adds +1%; Dow slips

The CME Group’s FedWatch Tool continues to project the Fed will hold the Federal Funds Rate steady in a target range of 5.25-5.50% until 1 May 2024 (2024-Q2). This date marks the anticipated beginning of a series of quarter point rate cuts that are expected to take place at six-to-twelve-week intervals through the end of 2024.

The Atlanta Fed’s GDPNow tool‘s latest estimate of real GDP growth for the first quarter of 2024 (2024-Q1) dropped to +3.4% from last week’s estimate of +4.2%.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.